Go Back

Last Updated :

Last Updated :

Mar 9, 2026

Mar 9, 2026

Form 1065 Schedule K-1: A Guide to Partnership Taxes

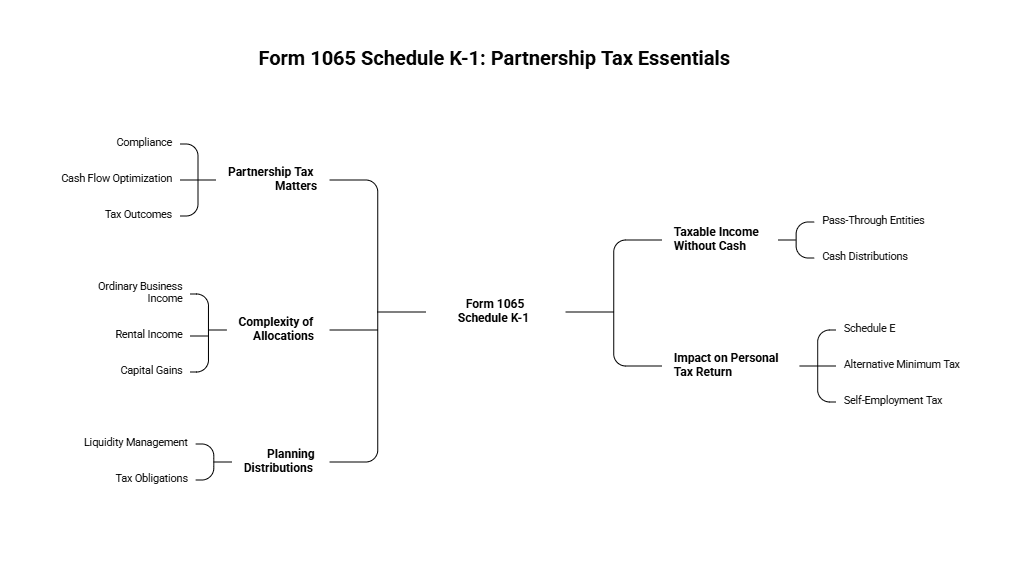

For those steering startups or managing partnerships, mastering the nuances of partnership tax matters is crucial—not just for compliance, but for optimizing cash flow and tax outcomes. One critical element encountered each year is the Form 1065 Schedule K-1, a tax document that often causes confusion and concern when it arrives in your mailbox.

This guide serves as a practical compass through the intricacies of Form 1065 Schedule K-1 and how partnership distributions influence your personal tax return. By the end, you’ll understand how to interpret the K-1, accurately report partnership income, and make smarter decisions around distributions to enhance your company’s financial health.

What Is Form 1065 Schedule K-1 and Why Does It Matter?

At its core, Form 1065 is the partnership’s annual tax return, similar in purpose to a corporate tax return but tailored specifically to pass-through entities that do not pay federal income tax themselves. Instead, the financial results pass directly to the partners via Schedule K-1.

Schedule K-1 (Form 1065) reports each partner’s share of profits, losses, deductions, and credits from the partnership during the tax year. As a founder and partner, even if the company did not distribute any cash to you, these allocated amounts are taxable on your individual return.

Taxable Income Without Cash: Partnerships are pass-through entities, so you’ll be taxed on profit allocations shown on your K-1 even if you didn’t receive a corresponding cash distribution.

Complexity of Allocations: Different types of income (ordinary business income, rental income, capital gains) have distinct tax treatments; misreporting can lead to penalties or missed tax planning opportunities.

Impact on Personal Tax Return: Schedule K-1 income integrates into various IRS forms such as Schedule E (Supplemental Income and Loss) and may influence alternative minimum tax (AMT) or self-employment tax liabilities.

Planning Distributions: Understanding the relationship between taxable income and actual partnership distributions is vital for managing liquidity and tax obligations.

For startups and agencies operating as partnerships or LLCs taxed as partnerships, decoding your Schedule K-1 is a foundational step toward clear financial visibility and strategic tax management.

Key Sections of the Schedule K-1

Schedule K-1 is divided into parts reporting different pieces of information essential for your personal tax return:

Section | Description | Impact |

Part I: Partnership Information | Basic partnership identification and tax year | Useful for verifying entity and tax year consistency |

Part II: Partner Information | Information about you as the partner | Ensures proper allocation and tax ID accuracy |

Part III: Partner’s Share of Income, Deductions, Credits, etc. | Details financial figures: - Box 1: Ordinary business income (loss) - Box 2: Net rental real estate income (loss) - Box 3: Other rental income (loss) - Box 12: Section 179 deduction | Direct impact on your tax liability and filing forms |

Key Boxes to Watch

Box 1: Ordinary Business Income (Loss)

This represents your share of the partnership’s profit or loss from active operations and is typically reported on Schedule E. It may also be subject to self-employment tax if you're an active partner.Box 2: Net Rental Real Estate Income (Loss)

Reflects your share of rental activities. Passive activity rules may limit your ability to deduct losses against other income.Box 12: Section 179 Deduction

Indicates expensing of depreciable property. This can be used to offset personal income when eligible.Other Boxes: Include interest income, dividend income, capital gains, and foreign transactions, each of which must be routed to its correct IRS tax schedules.

How Partnership Distributions Affect Your Personal Tax Return

Understanding the Distribution vs. Income Allocation Gap

One common source of confusion is the difference between taxable income allocated on the K-1 and cash distributions received:

You pay tax on the K-1 reported income, regardless of whether or not you received cash.

Cash distributions may not be taxable if they’re considered a return of capital.

Situation | Tax Treatment | Founder Considerations |

Taxable income allocated on K-1 | Report as income | Pay taxes even if you didn’t receive a check |

Distribution exceeds allocated income | Generally not taxable (return of capital) | Reduces your basis in the partnership |

Losses reported | May offset other income | Subject to at-risk and passive activity rules |

Tracking Your Basis in the Partnership

Your basis is the cumulative value of your investment in the partnership:

Basis = Initial contribution + Allocated income – Distributions – Losses

If distributions exceed your basis, the excess may trigger capital gains tax.

If losses exceed your basis, you may be unable to deduct them unless you’re personally liable for partnership debt.

Accurate basis tracking is essential. Many founders miss this step and incur unpleasant surprises when selling partnership interests or receiving outsized distributions.

Reporting Schedule K-1 Income on Your Return

Here’s a simple step-by-step guide you can follow:

Review your K-1 thoroughly. Confirm identity and capital percentages match your understanding.

Enter each item on the correct form:

Box 1 income ⇨ Schedule E

Self-employment earnings ⇨ Schedule SE

Interest/dividends/capital gains ⇨ Schedule B, Schedule D, or Form 8949

Rental info ⇨ Schedule E

Apply deductions and credits like Section 179 and R&D credits if shown on your K-1.

Update your basis calculations.

Attach the K-1 form with your return (electronically or mailed).

For detailed examples, visit the IRS instructions for Schedule K-1 (Form 1065).

Common K-1 Pitfalls and How to Navigate Them

Challenge | Explanation | Practical Action |

Late or amended K-1s | Partnerships may file extensions or corrections | File a personal return extension if necessary |

Opaque tax jargon | Tax details seem cryptic | Work with a tax advisor focused on partnerships |

Discrepancies between profit and cash | Taxable on profit even if no cash received | Regularly update basis and factor tax impact |

Loss limitations under passive activity rules | Passive incomes/losses face special limits | Determine your material participation level |

Strategic Tips to Optimize Partnership Tax Outcomes

Maintain real-time records of basis to track the taxability of distributions and use of losses.

Coordinate distributions with projected tax obligations to ensure cash is available to meet tax liabilities.

Explore deductions available via K-1, like Section 179, start-up cost amortizations, or energy investment credits.

Model the tax impact of major events such as conversions, partner buyouts, or equity raises.

Understand how Form 1065 Schedule K-1 informs other foundational planning areas, such as QSBS eligibility or merger structuring. For more on Qualified Small Business Stock, check our founder’s guide to QSBS.

Prepare for increasing IRS scrutiny under new audit rules for partnerships and track Form 8978 filings if audited. Learn about your compliance obligations in our Form 8978 article.

Make Form 1065 Schedule K-1 Work for You, Not Against You

Understanding and managing Form 1065 Schedule K-1 is pivotal for startup founders engaged in partnerships. It is the lens through which the IRS views your share of the business’s financials and directly impacts your personal tax landscape—whether or not cash made it to your pocket.

With clarity on what each part of the K-1 means, how to recognize tax opportunities and limits, and how your basis calculation affects taxability, you can empower yourself as a founder—not just to avoid tax drama, but to drive smarter business decisions and financial health.

For those steering startups or managing partnerships, mastering the nuances of partnership tax matters is crucial—not just for compliance, but for optimizing cash flow and tax outcomes. One critical element encountered each year is the Form 1065 Schedule K-1, a tax document that often causes confusion and concern when it arrives in your mailbox.

This guide serves as a practical compass through the intricacies of Form 1065 Schedule K-1 and how partnership distributions influence your personal tax return. By the end, you’ll understand how to interpret the K-1, accurately report partnership income, and make smarter decisions around distributions to enhance your company’s financial health.

What Is Form 1065 Schedule K-1 and Why Does It Matter?

At its core, Form 1065 is the partnership’s annual tax return, similar in purpose to a corporate tax return but tailored specifically to pass-through entities that do not pay federal income tax themselves. Instead, the financial results pass directly to the partners via Schedule K-1.

Schedule K-1 (Form 1065) reports each partner’s share of profits, losses, deductions, and credits from the partnership during the tax year. As a founder and partner, even if the company did not distribute any cash to you, these allocated amounts are taxable on your individual return.

Taxable Income Without Cash: Partnerships are pass-through entities, so you’ll be taxed on profit allocations shown on your K-1 even if you didn’t receive a corresponding cash distribution.

Complexity of Allocations: Different types of income (ordinary business income, rental income, capital gains) have distinct tax treatments; misreporting can lead to penalties or missed tax planning opportunities.

Impact on Personal Tax Return: Schedule K-1 income integrates into various IRS forms such as Schedule E (Supplemental Income and Loss) and may influence alternative minimum tax (AMT) or self-employment tax liabilities.

Planning Distributions: Understanding the relationship between taxable income and actual partnership distributions is vital for managing liquidity and tax obligations.

For startups and agencies operating as partnerships or LLCs taxed as partnerships, decoding your Schedule K-1 is a foundational step toward clear financial visibility and strategic tax management.

Key Sections of the Schedule K-1

Schedule K-1 is divided into parts reporting different pieces of information essential for your personal tax return:

Section | Description | Impact |

Part I: Partnership Information | Basic partnership identification and tax year | Useful for verifying entity and tax year consistency |

Part II: Partner Information | Information about you as the partner | Ensures proper allocation and tax ID accuracy |

Part III: Partner’s Share of Income, Deductions, Credits, etc. | Details financial figures: - Box 1: Ordinary business income (loss) - Box 2: Net rental real estate income (loss) - Box 3: Other rental income (loss) - Box 12: Section 179 deduction | Direct impact on your tax liability and filing forms |

Key Boxes to Watch

Box 1: Ordinary Business Income (Loss)

This represents your share of the partnership’s profit or loss from active operations and is typically reported on Schedule E. It may also be subject to self-employment tax if you're an active partner.Box 2: Net Rental Real Estate Income (Loss)

Reflects your share of rental activities. Passive activity rules may limit your ability to deduct losses against other income.Box 12: Section 179 Deduction

Indicates expensing of depreciable property. This can be used to offset personal income when eligible.Other Boxes: Include interest income, dividend income, capital gains, and foreign transactions, each of which must be routed to its correct IRS tax schedules.

How Partnership Distributions Affect Your Personal Tax Return

Understanding the Distribution vs. Income Allocation Gap

One common source of confusion is the difference between taxable income allocated on the K-1 and cash distributions received:

You pay tax on the K-1 reported income, regardless of whether or not you received cash.

Cash distributions may not be taxable if they’re considered a return of capital.

Situation | Tax Treatment | Founder Considerations |

Taxable income allocated on K-1 | Report as income | Pay taxes even if you didn’t receive a check |

Distribution exceeds allocated income | Generally not taxable (return of capital) | Reduces your basis in the partnership |

Losses reported | May offset other income | Subject to at-risk and passive activity rules |

Tracking Your Basis in the Partnership

Your basis is the cumulative value of your investment in the partnership:

Basis = Initial contribution + Allocated income – Distributions – Losses

If distributions exceed your basis, the excess may trigger capital gains tax.

If losses exceed your basis, you may be unable to deduct them unless you’re personally liable for partnership debt.

Accurate basis tracking is essential. Many founders miss this step and incur unpleasant surprises when selling partnership interests or receiving outsized distributions.

Reporting Schedule K-1 Income on Your Return

Here’s a simple step-by-step guide you can follow:

Review your K-1 thoroughly. Confirm identity and capital percentages match your understanding.

Enter each item on the correct form:

Box 1 income ⇨ Schedule E

Self-employment earnings ⇨ Schedule SE

Interest/dividends/capital gains ⇨ Schedule B, Schedule D, or Form 8949

Rental info ⇨ Schedule E

Apply deductions and credits like Section 179 and R&D credits if shown on your K-1.

Update your basis calculations.

Attach the K-1 form with your return (electronically or mailed).

For detailed examples, visit the IRS instructions for Schedule K-1 (Form 1065).

Common K-1 Pitfalls and How to Navigate Them

Challenge | Explanation | Practical Action |

Late or amended K-1s | Partnerships may file extensions or corrections | File a personal return extension if necessary |

Opaque tax jargon | Tax details seem cryptic | Work with a tax advisor focused on partnerships |

Discrepancies between profit and cash | Taxable on profit even if no cash received | Regularly update basis and factor tax impact |

Loss limitations under passive activity rules | Passive incomes/losses face special limits | Determine your material participation level |

Strategic Tips to Optimize Partnership Tax Outcomes

Maintain real-time records of basis to track the taxability of distributions and use of losses.

Coordinate distributions with projected tax obligations to ensure cash is available to meet tax liabilities.

Explore deductions available via K-1, like Section 179, start-up cost amortizations, or energy investment credits.

Model the tax impact of major events such as conversions, partner buyouts, or equity raises.

Understand how Form 1065 Schedule K-1 informs other foundational planning areas, such as QSBS eligibility or merger structuring. For more on Qualified Small Business Stock, check our founder’s guide to QSBS.

Prepare for increasing IRS scrutiny under new audit rules for partnerships and track Form 8978 filings if audited. Learn about your compliance obligations in our Form 8978 article.

Make Form 1065 Schedule K-1 Work for You, Not Against You

Understanding and managing Form 1065 Schedule K-1 is pivotal for startup founders engaged in partnerships. It is the lens through which the IRS views your share of the business’s financials and directly impacts your personal tax landscape—whether or not cash made it to your pocket.

With clarity on what each part of the K-1 means, how to recognize tax opportunities and limits, and how your basis calculation affects taxability, you can empower yourself as a founder—not just to avoid tax drama, but to drive smarter business decisions and financial health.

This article was co-written by:

Content

This article was co-written by:

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.