Go Back

Last Updated :

Last Updated :

Mar 20, 2026

Mar 20, 2026

Form 990 Schedule A: Nonprofit Compliance and Public Support Reporting

Running a startup, an e-commerce business, or an agency with nonprofit arms can quickly lead you into the intricacies of IRS filings, of which Form 990 Schedule A is a critical but often misunderstood requirement. For founders and finance leaders, mastering this filing ensures your organization maintains federal tax-exempt status, stays compliant, and transparently demonstrates public support—key for fundraising credibility and legal standing.

This guide breaks down Form 990 Schedule A from a founder’s perspective, focusing on what it is, who must file it, how to approach the public support test, and why bookkeeping accuracy and accounting consistency are essential. Whether your nonprofit is a standalone 501(c)(3) or a supporting organization, this article equips you to make confident, business-smart filing decisions—minimizing compliance risk and maximizing strategic insights.

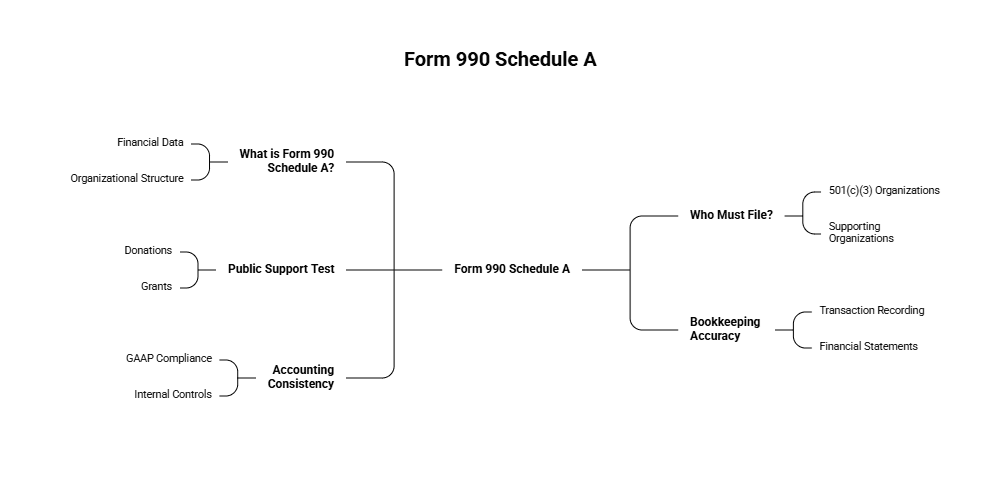

What Is Form 990 Schedule A and Why Is It Essential?

Form 990 Schedule A is an attachment to the IRS Form 990 used by many tax-exempt organizations to report detailed public support and other information supporting their qualification for tax exemption under IRS rules, primarily for 501(c)(3) organizations.

Key Reasons Founders Should Pay Attention:

Maintaining tax-exempt status: Failing to file Schedule A when required, or filing inaccurate data, can jeopardize your exemption.

Demonstrating public support: Schedule A includes the ""public support test,"" which assesses whether your nonprofit is supported predominantly by the public or private interests.

Transparency and accountability: It's a public document and helps stakeholders and donors understand your funding sources and compliance posture.

Strategic fundraising insights: Identifying trends in donor support types can inform your fundraising and partnership strategies.

Who Needs to File It?

Most 501(c)(3) organizations and certain other organizations exempt under sections like 509(a)(1), 509(a)(2), and 509(a)(3) must file Schedule A along with Form 990 or Form 990-EZ. However:

Churches and certain governmental organizations are generally exempt.

Some smaller nonprofits with gross receipts normally $50,000 or less file Form 990-N instead and do not file Schedule A.

To confirm organizational filing requirements for your specific nonprofit type, review the IRS official guidance on exempt organizations.

Understanding the Parts and Filing of Form 990 Schedule A

Form 990 Schedule A is divided into various parts covering different areas of reporting:

Part | Purpose | Who Files |

I | Public Support Schedule for 509(a)(1) and 170(b)(1)(A)(vi) nonprofits | Most public charities |

II | Public Support Schedule for 509(a)(2) organizations | Orgs receiving support primarily from gross receipts and services |

III | Supporting Organizations Information (509(a)(3) types) | Nonprofits classified as supporting organizations |

IV | Checklist of Required Schedules | All filers compiling necessary documentation |

V | Supplementary Information About Public Support | Case-specific disclosures and context |

How to Complete Key Sections

Part I & II: Report public support by year (e.g., contributions, grants, gov’t support). These numbers reveal if you meet the required public support thresholds.

Part III: Supporting organizations elaborate on their relationships and operational guidelines.

Parts IV & V: Internal reviews and narrative clarifications complete the documentation.

Recommendation for Founders: Track contributions and grants in real time using nonprofit-capable bookkeeping tools. Adopt systems that tag donations and revenue sources according to IRS definitions. These practices don't just simplify the year-end process—they defend against audits.

For assistance with extension filings, it’s important to understand IRS Form 8868.

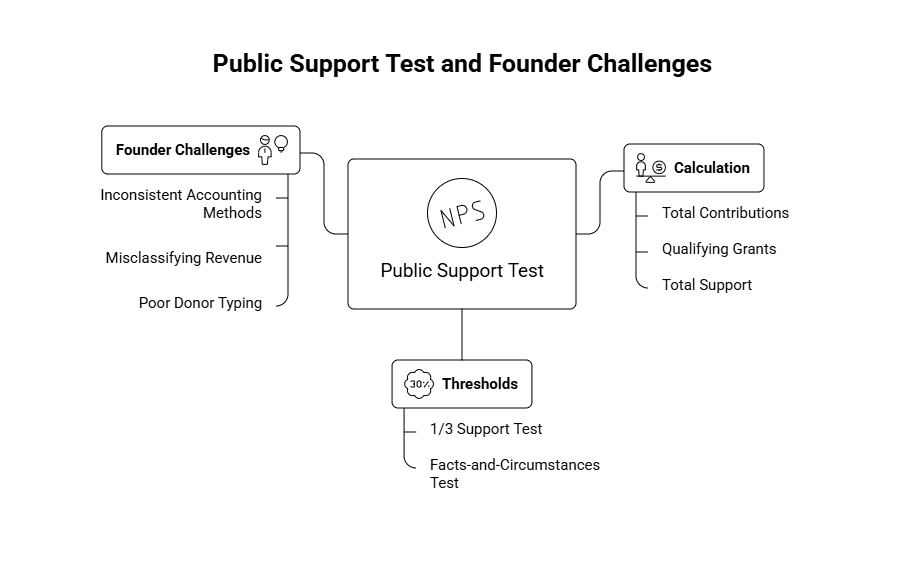

The Public Support Test: What Founders Must Understand

At the heart of Schedule A lies the public support test—a calculation that determines if your nonprofit receives adequate public funding to remain classified as a public charity rather than being reclassified as a private foundation.

How Public Support Percentage Is Calculated

Add total contributions and qualifying grants from public sources over a five-year rolling period.

Divide by total support, which includes revenue from all other sources, like investment income and unrelated business income.

The resulting percentage shows the degree to which your nonprofit is publicly supported.

Thresholds to Know

Test Type | Required Public Support % | Notes |

1/3 Support Test | At least 33 1/3% | Standard qualifying metric for many public charities |

Facts-and-Circumstances Test | Less than 33 1/3%, but IRS-approved justification | Special case based on totality of donor sources and operations |

Failing both can lead to private foundation designation, limiting your operational freedom and increasing scrutiny.

Common Founder Challenges with Schedule A and Bookkeeping Tips

1. Inconsistent Accounting Methods

Switching between cash and accrual accounting without properly noting it can confuse reporting and draw attention from the IRS.

Tip: Codify your accounting method in your bylaws or policies. If you must switch, clearly declare this on Form 990-to-IRS correspondence.

2. Misclassifying Revenue and Support

Distinguishing qualifying support from nonqualifying revenue is critical:

Government grants = generally count as public support

Program service revenue = may not count

Insider donations = may be capped or excluded

Tip: Use nonprofit-savvy software or a well-structured chart of accounts reflecting IRS definitions. Work with a CPA firm familiar with nonprofit regulations.

3. Poor Donor Typing and Reporting

Schedule A reveals whether your nonprofit’s funding is diverse or overly reliant on major donors.

Tip: Employ CRM and nonprofit fundraising tools that segment donor types and tie into financial systems.

Filing Process and Tools That Work for Startup Founders

When and How to File

Form 990 with Schedule A is due the 15th day of the 5th month post-fiscal year-end (e.g., May 15 for calendar year).

Filing extensions using Form 8868 are available.

Electronic submission is increasingly preferred and more trackable.

Startup founders often turn to fractional financial service providers that combine cloud-based accounting and nonprofit tax expertise. These teams handle IRS compliance and create funder-ready reports aligned with Schedule A metrics.

What to Do If You Fail the Public Support Test?

In the event your nonprofit fails the public support test, steps must be taken quickly to mitigate consequences and preserve your entity’s operational viability.

Founder Next Steps:

Immediately consult a tax-exempt specialist

Reevaluate fundraising approach to increase qualifying public support

Confirm that accounting methods and donor classification haven’t inadvertently underreported true public support

If warranted, seek IRS consideration under the facts-and-circumstances route

Form 990 Schedule A Helps Strengthen Nonprofit Foundations

For startup founders and finance leaders managing tax-exempt entities, Form 990 Schedule A is more than a compliance checkbox—it's a strategic tool demonstrating your public value and enabling credible fundraising. Accurate bookkeeping, proper public support tracking, and consistent accounting practices are essential to prevent reclassification and compliance issues.

Invest in expert nonprofit bookkeeping and use systems tailored to IRS expectations—it’s a smart, founder-friendly way to simplify tax season and unlock insights for growth.

Running a startup, an e-commerce business, or an agency with nonprofit arms can quickly lead you into the intricacies of IRS filings, of which Form 990 Schedule A is a critical but often misunderstood requirement. For founders and finance leaders, mastering this filing ensures your organization maintains federal tax-exempt status, stays compliant, and transparently demonstrates public support—key for fundraising credibility and legal standing.

This guide breaks down Form 990 Schedule A from a founder’s perspective, focusing on what it is, who must file it, how to approach the public support test, and why bookkeeping accuracy and accounting consistency are essential. Whether your nonprofit is a standalone 501(c)(3) or a supporting organization, this article equips you to make confident, business-smart filing decisions—minimizing compliance risk and maximizing strategic insights.

What Is Form 990 Schedule A and Why Is It Essential?

Form 990 Schedule A is an attachment to the IRS Form 990 used by many tax-exempt organizations to report detailed public support and other information supporting their qualification for tax exemption under IRS rules, primarily for 501(c)(3) organizations.

Key Reasons Founders Should Pay Attention:

Maintaining tax-exempt status: Failing to file Schedule A when required, or filing inaccurate data, can jeopardize your exemption.

Demonstrating public support: Schedule A includes the ""public support test,"" which assesses whether your nonprofit is supported predominantly by the public or private interests.

Transparency and accountability: It's a public document and helps stakeholders and donors understand your funding sources and compliance posture.

Strategic fundraising insights: Identifying trends in donor support types can inform your fundraising and partnership strategies.

Who Needs to File It?

Most 501(c)(3) organizations and certain other organizations exempt under sections like 509(a)(1), 509(a)(2), and 509(a)(3) must file Schedule A along with Form 990 or Form 990-EZ. However:

Churches and certain governmental organizations are generally exempt.

Some smaller nonprofits with gross receipts normally $50,000 or less file Form 990-N instead and do not file Schedule A.

To confirm organizational filing requirements for your specific nonprofit type, review the IRS official guidance on exempt organizations.

Understanding the Parts and Filing of Form 990 Schedule A

Form 990 Schedule A is divided into various parts covering different areas of reporting:

Part | Purpose | Who Files |

I | Public Support Schedule for 509(a)(1) and 170(b)(1)(A)(vi) nonprofits | Most public charities |

II | Public Support Schedule for 509(a)(2) organizations | Orgs receiving support primarily from gross receipts and services |

III | Supporting Organizations Information (509(a)(3) types) | Nonprofits classified as supporting organizations |

IV | Checklist of Required Schedules | All filers compiling necessary documentation |

V | Supplementary Information About Public Support | Case-specific disclosures and context |

How to Complete Key Sections

Part I & II: Report public support by year (e.g., contributions, grants, gov’t support). These numbers reveal if you meet the required public support thresholds.

Part III: Supporting organizations elaborate on their relationships and operational guidelines.

Parts IV & V: Internal reviews and narrative clarifications complete the documentation.

Recommendation for Founders: Track contributions and grants in real time using nonprofit-capable bookkeeping tools. Adopt systems that tag donations and revenue sources according to IRS definitions. These practices don't just simplify the year-end process—they defend against audits.

For assistance with extension filings, it’s important to understand IRS Form 8868.

The Public Support Test: What Founders Must Understand

At the heart of Schedule A lies the public support test—a calculation that determines if your nonprofit receives adequate public funding to remain classified as a public charity rather than being reclassified as a private foundation.

How Public Support Percentage Is Calculated

Add total contributions and qualifying grants from public sources over a five-year rolling period.

Divide by total support, which includes revenue from all other sources, like investment income and unrelated business income.

The resulting percentage shows the degree to which your nonprofit is publicly supported.

Thresholds to Know

Test Type | Required Public Support % | Notes |

1/3 Support Test | At least 33 1/3% | Standard qualifying metric for many public charities |

Facts-and-Circumstances Test | Less than 33 1/3%, but IRS-approved justification | Special case based on totality of donor sources and operations |

Failing both can lead to private foundation designation, limiting your operational freedom and increasing scrutiny.

Common Founder Challenges with Schedule A and Bookkeeping Tips

1. Inconsistent Accounting Methods

Switching between cash and accrual accounting without properly noting it can confuse reporting and draw attention from the IRS.

Tip: Codify your accounting method in your bylaws or policies. If you must switch, clearly declare this on Form 990-to-IRS correspondence.

2. Misclassifying Revenue and Support

Distinguishing qualifying support from nonqualifying revenue is critical:

Government grants = generally count as public support

Program service revenue = may not count

Insider donations = may be capped or excluded

Tip: Use nonprofit-savvy software or a well-structured chart of accounts reflecting IRS definitions. Work with a CPA firm familiar with nonprofit regulations.

3. Poor Donor Typing and Reporting

Schedule A reveals whether your nonprofit’s funding is diverse or overly reliant on major donors.

Tip: Employ CRM and nonprofit fundraising tools that segment donor types and tie into financial systems.

Filing Process and Tools That Work for Startup Founders

When and How to File

Form 990 with Schedule A is due the 15th day of the 5th month post-fiscal year-end (e.g., May 15 for calendar year).

Filing extensions using Form 8868 are available.

Electronic submission is increasingly preferred and more trackable.

Startup founders often turn to fractional financial service providers that combine cloud-based accounting and nonprofit tax expertise. These teams handle IRS compliance and create funder-ready reports aligned with Schedule A metrics.

What to Do If You Fail the Public Support Test?

In the event your nonprofit fails the public support test, steps must be taken quickly to mitigate consequences and preserve your entity’s operational viability.

Founder Next Steps:

Immediately consult a tax-exempt specialist

Reevaluate fundraising approach to increase qualifying public support

Confirm that accounting methods and donor classification haven’t inadvertently underreported true public support

If warranted, seek IRS consideration under the facts-and-circumstances route

Form 990 Schedule A Helps Strengthen Nonprofit Foundations

For startup founders and finance leaders managing tax-exempt entities, Form 990 Schedule A is more than a compliance checkbox—it's a strategic tool demonstrating your public value and enabling credible fundraising. Accurate bookkeeping, proper public support tracking, and consistent accounting practices are essential to prevent reclassification and compliance issues.

Invest in expert nonprofit bookkeeping and use systems tailored to IRS expectations—it’s a smart, founder-friendly way to simplify tax season and unlock insights for growth.

This article was co-written by:

Content

This article was co-written by:

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.