Go Back

Last Updated :

Last Updated :

Jan 26, 2026

Jan 26, 2026

Form W-8BEN: A Compliance Guide for Non-U.S. Businesses

For founders running startups, agencies, or ecommerce businesses with international relationships, understanding Form W-8BEN is essential for managing U.S. withholding tax compliance.

Form W-8BEN is used by foreign individuals to certify their non-U.S. status when receiving certain types of U.S.-source income. When collected correctly, it allows you to apply the proper withholding rate—and, in some cases, reduce or eliminate withholding under an applicable tax treaty.

In this guide, we explain what Form W-8BEN is, who needs to complete it, when it’s required, and how founders should manage it as part of a clean, audit-ready finance operation.

What Is Form W-8BEN—and Why It Matters

Form W-8BEN, officially titled Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting, is completed by non-U.S. individuals who receive certain types of income from U.S. sources.

Common income types include:

Dividends

Royalties

Interest

Other fixed or determinable passive income

The form tells the payer:

The individual is not a U.S. person

Whether a tax treaty applies

What withholding rate should be applied

Without a valid W-8BEN on file, U.S. payers are generally required to withhold 30% on applicable income by default.

Why Founders Should Care

As a founder, you typically don’t file Form W-8BEN—but you are often responsible for collecting and retaining it.

This commonly applies when you:

Pay royalties to individuals located outside the U.S.

Make distributions or other payments to foreign investors

Work with international consultants where income characterization requires documentation

Having a valid W-8BEN helps ensure:

Correct withholding is applied

Treaty benefits are honored when applicable

Your company stays compliant and audit-ready

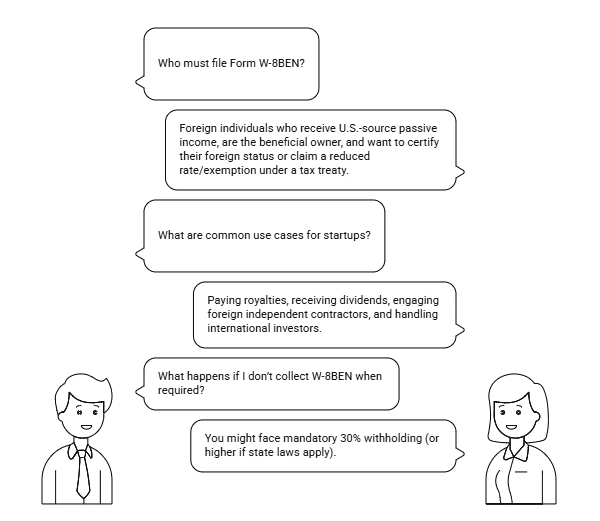

Who Must File Form W-8BEN?

Form W-8BEN must be completed by foreign individuals who:

Are the beneficial owner of the income

Receive U.S.-source income

Want to avoid the default 30% withholding or claim treaty benefits

Important note for contractors:

Services performed entirely outside the U.S. are generally not U.S.-source income. In those cases, withholding may not apply—but many companies still require a W-8BEN from consultants for documentation and to maintain compliance with requirements.

Completing Form W-8BEN: What Founders Should Review

While the foreign individual completes the form, founders should understand the key sections:

Section | What It Covers | Founder Check |

Part I | Identity and country of citizenship | Confirm country matches treaty claim |

Part II | Tax treaty benefits | Ensure treaty article and rate are specified |

Part III | Certification | Verify signature and date |

Forms should be provided to you or your payment processor, not sent to the IRS.

Validity and Renewal Rules

Form W-8BEN is valid for three full calendar years after signing

Expired forms trigger default 30% withholding

Track expirations to avoid payment delays or compliance gaps

W-8BEN vs Other W-8 Forms

W-8BEN: Foreign individuals

W-8BEN-E: Foreign entities

W-8ECI: Income connected to U.S. business activity

W-8IMY: Intermediaries or flow-through entities

Using the wrong form is a common—and avoidable—error.

How Form W-8BEN Fits Into a Clean Finance Stack

While Form W-8BEN doesn’t directly impact tax credits, it plays a supporting role in:

Clean expense documentation

Accurate withholding treatment

Audit-ready financial reporting

If you rely on international talent or partners, consistent W-8BEN management reduces friction across payroll, AP, and tax reporting.

What Happens If You Don’t File or Submit Form W-8BEN?

If a required Form W-8BEN is not provided, the payer is generally required to withhold tax at the default 30% U.S. withholding rate on applicable U.S.-source income paid to a foreign individual.

In some cases, missing or invalid documentation can also cause payers or payment platforms to withhold by default until proper forms are on file, delaying payments and creating cash-flow issues.

Providing a valid Form W-8BEN on time allows the payer to:

Apply the correct withholding rate

Honor any applicable tax treaty benefits

Avoid unnecessary over-withholding and payment disruptions

Founder Takeaway

Owning W-8BEN compliance helps you:

Avoid over-withholding or payment delays

Apply treaty benefits correctly

Keep your books clean and defensible

It’s a small form—but one that protects your cash flow and compliance posture as your business scales.

For founders running startups, agencies, or ecommerce businesses with international relationships, understanding Form W-8BEN is essential for managing U.S. withholding tax compliance.

Form W-8BEN is used by foreign individuals to certify their non-U.S. status when receiving certain types of U.S.-source income. When collected correctly, it allows you to apply the proper withholding rate—and, in some cases, reduce or eliminate withholding under an applicable tax treaty.

In this guide, we explain what Form W-8BEN is, who needs to complete it, when it’s required, and how founders should manage it as part of a clean, audit-ready finance operation.

What Is Form W-8BEN—and Why It Matters

Form W-8BEN, officially titled Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting, is completed by non-U.S. individuals who receive certain types of income from U.S. sources.

Common income types include:

Dividends

Royalties

Interest

Other fixed or determinable passive income

The form tells the payer:

The individual is not a U.S. person

Whether a tax treaty applies

What withholding rate should be applied

Without a valid W-8BEN on file, U.S. payers are generally required to withhold 30% on applicable income by default.

Why Founders Should Care

As a founder, you typically don’t file Form W-8BEN—but you are often responsible for collecting and retaining it.

This commonly applies when you:

Pay royalties to individuals located outside the U.S.

Make distributions or other payments to foreign investors

Work with international consultants where income characterization requires documentation

Having a valid W-8BEN helps ensure:

Correct withholding is applied

Treaty benefits are honored when applicable

Your company stays compliant and audit-ready

Who Must File Form W-8BEN?

Form W-8BEN must be completed by foreign individuals who:

Are the beneficial owner of the income

Receive U.S.-source income

Want to avoid the default 30% withholding or claim treaty benefits

Important note for contractors:

Services performed entirely outside the U.S. are generally not U.S.-source income. In those cases, withholding may not apply—but many companies still require a W-8BEN from consultants for documentation and to maintain compliance with requirements.

Completing Form W-8BEN: What Founders Should Review

While the foreign individual completes the form, founders should understand the key sections:

Section | What It Covers | Founder Check |

Part I | Identity and country of citizenship | Confirm country matches treaty claim |

Part II | Tax treaty benefits | Ensure treaty article and rate are specified |

Part III | Certification | Verify signature and date |

Forms should be provided to you or your payment processor, not sent to the IRS.

Validity and Renewal Rules

Form W-8BEN is valid for three full calendar years after signing

Expired forms trigger default 30% withholding

Track expirations to avoid payment delays or compliance gaps

W-8BEN vs Other W-8 Forms

W-8BEN: Foreign individuals

W-8BEN-E: Foreign entities

W-8ECI: Income connected to U.S. business activity

W-8IMY: Intermediaries or flow-through entities

Using the wrong form is a common—and avoidable—error.

How Form W-8BEN Fits Into a Clean Finance Stack

While Form W-8BEN doesn’t directly impact tax credits, it plays a supporting role in:

Clean expense documentation

Accurate withholding treatment

Audit-ready financial reporting

If you rely on international talent or partners, consistent W-8BEN management reduces friction across payroll, AP, and tax reporting.

What Happens If You Don’t File or Submit Form W-8BEN?

If a required Form W-8BEN is not provided, the payer is generally required to withhold tax at the default 30% U.S. withholding rate on applicable U.S.-source income paid to a foreign individual.

In some cases, missing or invalid documentation can also cause payers or payment platforms to withhold by default until proper forms are on file, delaying payments and creating cash-flow issues.

Providing a valid Form W-8BEN on time allows the payer to:

Apply the correct withholding rate

Honor any applicable tax treaty benefits

Avoid unnecessary over-withholding and payment disruptions

Founder Takeaway

Owning W-8BEN compliance helps you:

Avoid over-withholding or payment delays

Apply treaty benefits correctly

Keep your books clean and defensible

It’s a small form—but one that protects your cash flow and compliance posture as your business scales.

This article was co-written by:

Content

This article was co-written by:

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.