Go Back

Last Updated :

Last Updated :

Mar 20, 2026

Mar 20, 2026

Form 990-T: Managing Unrelated Business Income (UBI) for Nonprofits without Losing Tax-Exempt Status

Nonprofits frequently navigate complex financial landscapes, balancing mission-driven initiatives with operational necessities. One nuanced area that often trips up even experienced founders and finance leaders is unrelated business income (UBI). How you manage this income can influence not just your bottom line but also your nonprofit’s hard-earned tax-exempt status. At the heart of compliance lies Form 990-T, the IRS form for reporting and paying tax on UBI.

This guide offers a founder-friendly roadmap for managing UBI for nonprofits, explaining what it is, how it affects tax-exempt status, and practical strategies to handle it without jeopardizing your organization’s status.

What Is Unrelated Business Income?

Unrelated Business Income (UBI) is income generated from activities that are not substantially related to your nonprofit’s primary exempt purpose, yet they are regularly carried on like a business. For example:

A charity operating a gift shop selling unrelated merchandise

A nonprofit running a parking lot open to the general public

Rental income from debt-financed property (even if related to your organization's mission)

The IRS taxes UBI to prevent nonprofits from gaining unfair competitive advantages over taxable businesses. While your nonprofit enjoys tax-exempt status on mission-related income, UBI is taxable, and if not properly managed and reported, it can jeopardize your exemption.

Understanding Form 990-T: What Nonprofits Need to Know

Form 990-T (“Exempt Organization Business Income Tax Return”) is the IRS form exempt organizations use to report unrelated business taxable income (UBTI) and compute income tax owed on that income.

Who Must File Form 990-T?

Your nonprofit must file this form if it:

Has gross income of $1,000 or more from unrelated business activities during the tax year

Recognizes unrelated debt-financed income (income from property financed by borrowed funds)

Wants to claim specific tax credits related to UBI

Important: Even if the organization owes zero tax because its deductions equal UBI, it generally must still file Form 990-T to report the activity. Not filing can lead to IRS penalties or increased scrutiny, which puts your exemption at risk.

When Is Form 990-T Due?

Typically due by the 15th day of the 5th month after the close of the tax year (May 15 for calendar-year filers)

Extensions are possible by filing Form 8868

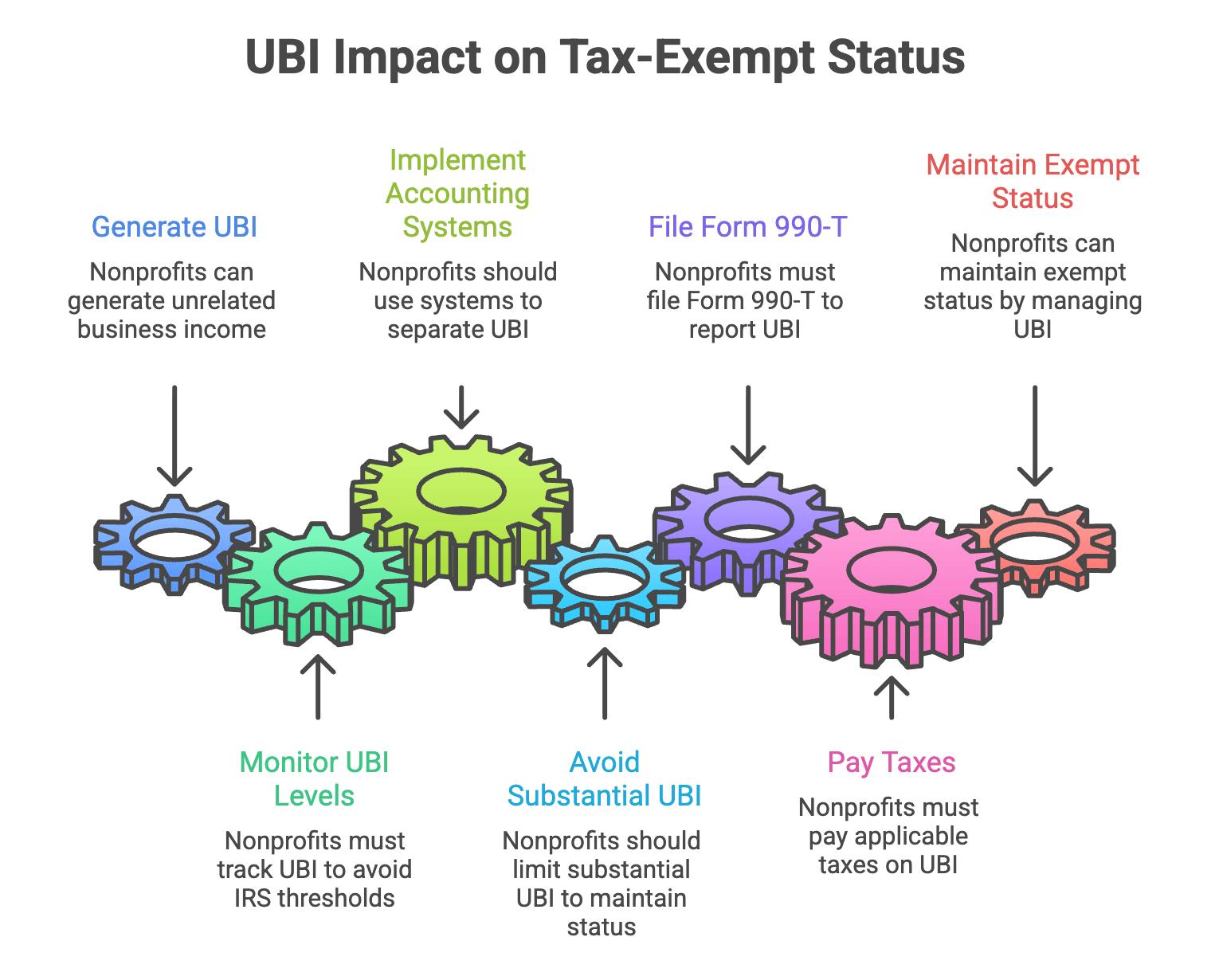

How Unrelated Business Income Impacts Tax-Exempt Status

UBI itself does not automatically jeopardize your nonprofit’s tax-exempt status. Nonprofits are allowed to generate unrelated business income — the IRS understands organizations must sometimes supplement mission-related revenue.

However:

Repeated, substantial unrelated business activity can trigger loss of exemption if the IRS determines the business is no longer operated primarily for exempt purposes.

Failure to file Form 990-T and pay applicable taxes can result in penalties, liens, or even revocation.

If your nonprofit receives too much income from unrelated sources (depending on the magnitude and pattern), the IRS may reassess your exemption during audits.

Practical Insights

Balance is key. It’s vital to actively monitor the portion of your revenue and activities that fall into the unrelated category to avoid crossing IRS thresholds. Founders should implement accounting tracking systems that clearly separate unrelated business activities from exempt functions. This level of financial clarity both empowers strategic decision-making and satisfies IRS oversight.

Common Sources of Unrelated Business Income for Startups and Agencies

Founders leading startups, agencies, or ecommerce nonprofits may encounter UBI from:

Activity | UBI Example | Notes |

Selling goods unrelated to exempt mission | Merchandise sales unrelated to nonprofit cause | May create UBI if regularly conducted |

Advertising income | Selling ad space on your website | Generally considered UBI unless it’s incidental or related |

Rental income from debt-financed property | Office space rented to third parties | Treated as UBI even if related to mission |

Services performed for a fee unrelated to mission | Providing consulting to for-profit clients | UBI, unless “substantially related” to exempt purpose |

How to File Form 990-T: A Step-by-Step Guide

Filing Form 990-T may seem daunting, but taking it step-by-step and enlisting expert bookkeeping support can prevent costly errors.

1. Identify and Segregate UBI in Your Accounting System

Track income from unrelated activities separately

Maintain documentation clearly tying income to UBI activities

Use categories/classes in your bookkeeping software for itemization

2. Calculate Gross Income from Unrelated Business Activities

Sum all income generated regularly from unrelated trades or businesses.

3. Subtract Allowable Deductions Directly Connected to UBI

Deduct expenses that are ordinary, necessary, and directly connected to producing UBI:

Cost of goods sold

Employee wages related to the unrelated business

Rent or utilities for spaces used exclusively in unrelated business

Note: General administrative expenses for the entire organization are typically not deductible.

4. Determine Net Unrelated Business Taxable Income (UBTI)

Gross income minus allowable deductions equals your taxable UBI.

5. Calculate Tax Liability

Corporations generally pay tax at standard corporate rates on UBTI. Trusts and IRAs have a different schedule.

6. Complete and File Form 990-T

File even if your UBTI results in zero tax (due to deductions)

Electronically file if required by the IRS; paper filing is still accepted in many cases

Apply for extension using Form 8868 if necessary

Best Practices to Manage UBI Without Risking Tax-Exempt Status

Monitor UBI thresholds regularly

Set internal reports to review unrelated revenue quarterly or monthly. It’s easier to recalibrate activities early rather than face IRS penalties or audits.

Maintain clear documentation

Detailed records that validate which income streams are UBI and associated expenses will safeguard your filings during any IRS inquiries.

Separate unrelated activities operationally and financially

When feasible, run unrelated business activities in separate entities or divisions to insulate your nonprofit’s exempt functions.

Common Questions About UBI and Form 990-T

Question | Answer |

What if my nonprofit has passive income? | Passive income, such as dividends or interest, generally is not UBI and not subject to Form 990-T (unless debt-financed). |

Can nonprofits claim tax credits on Form 990-T? | Yes. Certain credits, such as the general business credit, can be claimed if applicable. |

Are there penalties for late or non-filing? | Yes. Penalties accrue for failure to file and pay UBI tax timely, which may compound IRS issues. |

Is electronic filing mandatory? | The IRS is moving toward mandatory electronic filing for Form 990-T. Currently, many nonprofits still file paper forms, but expect change. |

How Software and Services Can Simplify UBI Reporting

Modern nonprofit-focused accounting software can simplify the tracking and reporting of UBI. Look for features like:

Revenue categorization with custom tags for unrelated business income

Built-in reports for Form 990-T preparation

Seamless support for electronic filing

In addition, outsourced accounting and tax services help nonprofit founders reduce risk and reclaim time by providing expert insights and full-service compliance support.

Mastering UBI Compliance with Form 990-T

Understanding and managing unrelated business income (UBI) is a critical, yet often overlooked, responsibility for nonprofit founders. Filing Form 990-T correctly and on time ensures your organization complies with IRS requirements without risking your tax-exempt status.

Nonprofits frequently navigate complex financial landscapes, balancing mission-driven initiatives with operational necessities. One nuanced area that often trips up even experienced founders and finance leaders is unrelated business income (UBI). How you manage this income can influence not just your bottom line but also your nonprofit’s hard-earned tax-exempt status. At the heart of compliance lies Form 990-T, the IRS form for reporting and paying tax on UBI.

This guide offers a founder-friendly roadmap for managing UBI for nonprofits, explaining what it is, how it affects tax-exempt status, and practical strategies to handle it without jeopardizing your organization’s status.

What Is Unrelated Business Income?

Unrelated Business Income (UBI) is income generated from activities that are not substantially related to your nonprofit’s primary exempt purpose, yet they are regularly carried on like a business. For example:

A charity operating a gift shop selling unrelated merchandise

A nonprofit running a parking lot open to the general public

Rental income from debt-financed property (even if related to your organization's mission)

The IRS taxes UBI to prevent nonprofits from gaining unfair competitive advantages over taxable businesses. While your nonprofit enjoys tax-exempt status on mission-related income, UBI is taxable, and if not properly managed and reported, it can jeopardize your exemption.

Understanding Form 990-T: What Nonprofits Need to Know

Form 990-T (“Exempt Organization Business Income Tax Return”) is the IRS form exempt organizations use to report unrelated business taxable income (UBTI) and compute income tax owed on that income.

Who Must File Form 990-T?

Your nonprofit must file this form if it:

Has gross income of $1,000 or more from unrelated business activities during the tax year

Recognizes unrelated debt-financed income (income from property financed by borrowed funds)

Wants to claim specific tax credits related to UBI

Important: Even if the organization owes zero tax because its deductions equal UBI, it generally must still file Form 990-T to report the activity. Not filing can lead to IRS penalties or increased scrutiny, which puts your exemption at risk.

When Is Form 990-T Due?

Typically due by the 15th day of the 5th month after the close of the tax year (May 15 for calendar-year filers)

Extensions are possible by filing Form 8868

How Unrelated Business Income Impacts Tax-Exempt Status

UBI itself does not automatically jeopardize your nonprofit’s tax-exempt status. Nonprofits are allowed to generate unrelated business income — the IRS understands organizations must sometimes supplement mission-related revenue.

However:

Repeated, substantial unrelated business activity can trigger loss of exemption if the IRS determines the business is no longer operated primarily for exempt purposes.

Failure to file Form 990-T and pay applicable taxes can result in penalties, liens, or even revocation.

If your nonprofit receives too much income from unrelated sources (depending on the magnitude and pattern), the IRS may reassess your exemption during audits.

Practical Insights

Balance is key. It’s vital to actively monitor the portion of your revenue and activities that fall into the unrelated category to avoid crossing IRS thresholds. Founders should implement accounting tracking systems that clearly separate unrelated business activities from exempt functions. This level of financial clarity both empowers strategic decision-making and satisfies IRS oversight.

Common Sources of Unrelated Business Income for Startups and Agencies

Founders leading startups, agencies, or ecommerce nonprofits may encounter UBI from:

Activity | UBI Example | Notes |

Selling goods unrelated to exempt mission | Merchandise sales unrelated to nonprofit cause | May create UBI if regularly conducted |

Advertising income | Selling ad space on your website | Generally considered UBI unless it’s incidental or related |

Rental income from debt-financed property | Office space rented to third parties | Treated as UBI even if related to mission |

Services performed for a fee unrelated to mission | Providing consulting to for-profit clients | UBI, unless “substantially related” to exempt purpose |

How to File Form 990-T: A Step-by-Step Guide

Filing Form 990-T may seem daunting, but taking it step-by-step and enlisting expert bookkeeping support can prevent costly errors.

1. Identify and Segregate UBI in Your Accounting System

Track income from unrelated activities separately

Maintain documentation clearly tying income to UBI activities

Use categories/classes in your bookkeeping software for itemization

2. Calculate Gross Income from Unrelated Business Activities

Sum all income generated regularly from unrelated trades or businesses.

3. Subtract Allowable Deductions Directly Connected to UBI

Deduct expenses that are ordinary, necessary, and directly connected to producing UBI:

Cost of goods sold

Employee wages related to the unrelated business

Rent or utilities for spaces used exclusively in unrelated business

Note: General administrative expenses for the entire organization are typically not deductible.

4. Determine Net Unrelated Business Taxable Income (UBTI)

Gross income minus allowable deductions equals your taxable UBI.

5. Calculate Tax Liability

Corporations generally pay tax at standard corporate rates on UBTI. Trusts and IRAs have a different schedule.

6. Complete and File Form 990-T

File even if your UBTI results in zero tax (due to deductions)

Electronically file if required by the IRS; paper filing is still accepted in many cases

Apply for extension using Form 8868 if necessary

Best Practices to Manage UBI Without Risking Tax-Exempt Status

Monitor UBI thresholds regularly

Set internal reports to review unrelated revenue quarterly or monthly. It’s easier to recalibrate activities early rather than face IRS penalties or audits.

Maintain clear documentation

Detailed records that validate which income streams are UBI and associated expenses will safeguard your filings during any IRS inquiries.

Separate unrelated activities operationally and financially

When feasible, run unrelated business activities in separate entities or divisions to insulate your nonprofit’s exempt functions.

Common Questions About UBI and Form 990-T

Question | Answer |

What if my nonprofit has passive income? | Passive income, such as dividends or interest, generally is not UBI and not subject to Form 990-T (unless debt-financed). |

Can nonprofits claim tax credits on Form 990-T? | Yes. Certain credits, such as the general business credit, can be claimed if applicable. |

Are there penalties for late or non-filing? | Yes. Penalties accrue for failure to file and pay UBI tax timely, which may compound IRS issues. |

Is electronic filing mandatory? | The IRS is moving toward mandatory electronic filing for Form 990-T. Currently, many nonprofits still file paper forms, but expect change. |

How Software and Services Can Simplify UBI Reporting

Modern nonprofit-focused accounting software can simplify the tracking and reporting of UBI. Look for features like:

Revenue categorization with custom tags for unrelated business income

Built-in reports for Form 990-T preparation

Seamless support for electronic filing

In addition, outsourced accounting and tax services help nonprofit founders reduce risk and reclaim time by providing expert insights and full-service compliance support.

Mastering UBI Compliance with Form 990-T

Understanding and managing unrelated business income (UBI) is a critical, yet often overlooked, responsibility for nonprofit founders. Filing Form 990-T correctly and on time ensures your organization complies with IRS requirements without risking your tax-exempt status.

This article was co-written by:

Content

This article was co-written by:

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.