Go Back

Last Updated :

Last Updated :

Mar 9, 2026

Mar 9, 2026

Form 5405: Calculating and Reporting the Repayment of the First-Time Homebuyer Credit

For founders scaling startups, managing finances means knowing not only how to optimize taxes but also how to handle complex credits and repayments with confidence and clarity. One tax form that can cause uncertainty for taxpayers who claimed the First-Time Homebuyer Credit is Form 5405. Understanding when and how to file this form is essential to avoid unexpected tax liabilities and to maintain clean, compliant records.

In this article, we'll break down who needs to file Form 5405, guide you through the calculation of repayment, clarify exceptions, and share practical advice on reporting this on your tax returns.

What Is IRS Form 5405 and Who Must File It?

Form 5405, Repayment of the First-Time Homebuyer Credit, is the IRS tool used by taxpayers who claimed the First-Time Homebuyer Credit but later must repay part or all of it.

The credit was designed to encourage homeownership, but the IRS requires repayment in specific circumstances, often tied to selling or no longer using the home as your main residence.

When Do You Need to File Form 5405?

You must file this form when you claimed the First-Time Homebuyer Credit and any of the following apply:

You sold your home or transferred ownership before meeting the required ownership period (typically 36 months). company growth or rely on home equity loans, understanding potential repayment obligations helps avoid cash flow surprises

You no longer use the home as your main residence before fulfilling the ownership period.

You had to repay the credit due to other changes in your primary residence status as defined by IRS rules.

If none of these apply, and the conditions of the credit remain met, you generally do not need to file Form 5405.

Why Is This Important?

While this topic primarily affects individuals, you should be aware of the financial implications for themselves and any stakeholders. For example, if you claimed the credit on your personal tax return and later sell your home, you may face a repayment, which affects your personal tax position and liquidity.

For those who invest significant personal funds into company growth or rely on home equity loans, understanding potential repayment obligations avoids surprises in cash flow. Additionally, founders consulting their finance teams should ensure correct filing to keep personal and business tax matters separate and compliant.

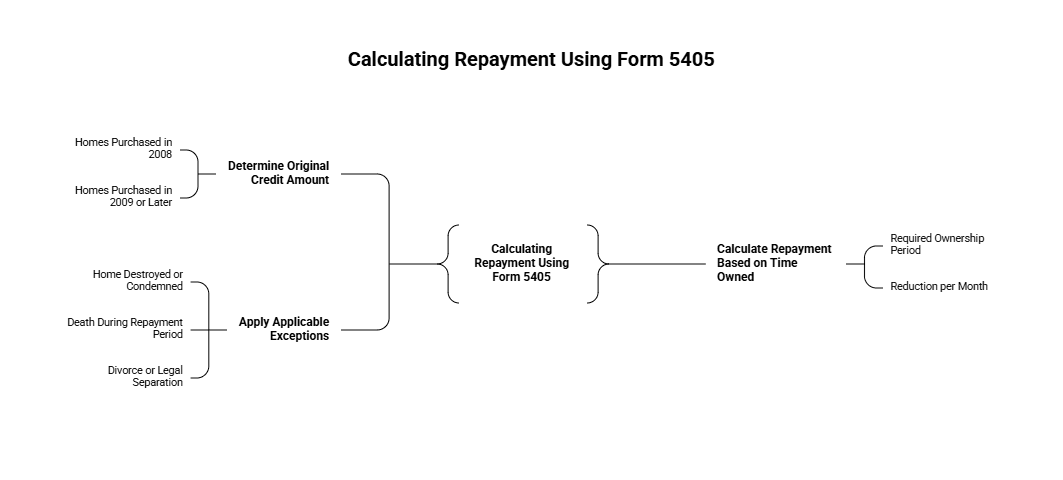

Calculating Your Repayment Using Form 5405

Understanding how to compute your repayment liability is critical to ensuring IRS compliance without overpaying. Let’s walk through the process step by step.

Step 1: Determine Your Original Credit Amount

Keep your tax documents handy to identify the exact credit amount you received. Generally:

$7,500 for homes purchased in 2008 (to be repaid in installments over 15 years).

$8,000 for homes purchased in 2009 or later (with a potential requirement to repay in full if requirements aren't met).

Step 2: Calculate the Repayment Based on Time Owned

Repayment is typically prorated based on how long you lived in the home before selling or changing residences.

Required ownership period: 36 months from date of purchase.

For every full month you fulfill the ownership requirement, you reduce what you owe by 1/36th.

For example:

Original Credit: $7,500

Months Owned: 18

Repayment = (36 - 18) / 36 = 50% of credit = $3,750

Step 3: Apply Any Applicable Exceptions

There are a few IRS-sanctioned exceptions to repayment:

The home was destroyed or condemned (e.g., by fire or natural disaster).

You died during the repayment period — no further repayments are due.

Divorce or legal separation resulting in the transfer of ownership.

You’ll need to document these exceptions, typically with legal or insurance paperwork.

Filing Form 5405: A Step-by-Step Guide

Whether you manage your own taxes or outsource your filings, knowing what to expect on Form 5405 helps reduce errors and delays.

Major Sections of Form 5405

Part I – Used to notify the IRS that you ceased using the home as your main residence.

Part II – Required if you sold the home and need to calculate repayment.

Part III – Used for exceptions or other specific events requiring disclosure.

Filing Tips

Attach Form 5405 to your annual Form 1040 tax return.

Include payment on Schedule 2 (Additional Taxes) if repayment applies.

Clearly report the sale date, credit received, and documentation of exceptions (if applicable).

Use bookkeeping platforms or document vaults to retain escrow statements, tax returns, proof of residence, and IRS letters.

Can You Avoid Repayment of the First-Time Homebuyer Credit?

Yes — under certain conditions, taxpayers can avoid repayment altogether. That’s good news if any of the following apply to your situation.

Common Exceptions That Waive Repayment

You converted the home to a rental after the 36-month period.

You transferred the home to a spouse or ex-spouse under a divorce agreement.

The home was destroyed or condemned, and you didn’t acquire a replacement residence within two years.

The taxpayer died before completing repayment (in which case, no further action is needed).

Documentation is essential. File any applicable statements with your return and maintain these records in case of IRS inquiry.

You can verify exception qualifications on the official IRS Form 5405 publication and instructions.

Common Mistakes To Avoid

With your time split between company growth and compliance details, mistakes can slip through. Here are the most common missteps related to Form 5405:

Mistake | Remedy |

Forgetting to file Form 5405 | Annually review changes in residence if you claimed the credit. |

Reporting incorrect ownership data | Cross-reference closing documents and utility bills. |

Filing late or omitting the form | File with your 1040 annually if required—IRS penalties can apply. |

Missed exceptions | Review IRS criteria or speak with a tax advisor before filing. |

What Comes Next? Actionable Steps for Startup Operators

Here’s what founders should do now to stay ahead of repayment:

Audit your own tax history – Confirm if you've ever claimed the First-Time Homebuyer Credit.

Review home sale or relocation dates – Match them against the 36-month rule.

Run the Form 5405 calculation if repayment is due, and identify any potential exceptions.

Work with a tax professional or use founder-focused platforms to automate this as part of your finance process.

If you’re relying on personal liquidity or creditworthiness to support your startup, compliant and transparent tax records keep you ready for your next raise, audit, or investment round.

Mastering Form 5405 Is About Protecting Your Startup’s Future

Form 5405 plays a critical role in calculating and reporting repayment of the First-Time Homebuyer Credit. If you’ve sold your home or changed residences after claiming this credit, understanding your filing obligations prevents costly surprises from disrupting your personal or business finances.

For founders scaling startups, managing finances means knowing not only how to optimize taxes but also how to handle complex credits and repayments with confidence and clarity. One tax form that can cause uncertainty for taxpayers who claimed the First-Time Homebuyer Credit is Form 5405. Understanding when and how to file this form is essential to avoid unexpected tax liabilities and to maintain clean, compliant records.

In this article, we'll break down who needs to file Form 5405, guide you through the calculation of repayment, clarify exceptions, and share practical advice on reporting this on your tax returns.

What Is IRS Form 5405 and Who Must File It?

Form 5405, Repayment of the First-Time Homebuyer Credit, is the IRS tool used by taxpayers who claimed the First-Time Homebuyer Credit but later must repay part or all of it.

The credit was designed to encourage homeownership, but the IRS requires repayment in specific circumstances, often tied to selling or no longer using the home as your main residence.

When Do You Need to File Form 5405?

You must file this form when you claimed the First-Time Homebuyer Credit and any of the following apply:

You sold your home or transferred ownership before meeting the required ownership period (typically 36 months). company growth or rely on home equity loans, understanding potential repayment obligations helps avoid cash flow surprises

You no longer use the home as your main residence before fulfilling the ownership period.

You had to repay the credit due to other changes in your primary residence status as defined by IRS rules.

If none of these apply, and the conditions of the credit remain met, you generally do not need to file Form 5405.

Why Is This Important?

While this topic primarily affects individuals, you should be aware of the financial implications for themselves and any stakeholders. For example, if you claimed the credit on your personal tax return and later sell your home, you may face a repayment, which affects your personal tax position and liquidity.

For those who invest significant personal funds into company growth or rely on home equity loans, understanding potential repayment obligations avoids surprises in cash flow. Additionally, founders consulting their finance teams should ensure correct filing to keep personal and business tax matters separate and compliant.

Calculating Your Repayment Using Form 5405

Understanding how to compute your repayment liability is critical to ensuring IRS compliance without overpaying. Let’s walk through the process step by step.

Step 1: Determine Your Original Credit Amount

Keep your tax documents handy to identify the exact credit amount you received. Generally:

$7,500 for homes purchased in 2008 (to be repaid in installments over 15 years).

$8,000 for homes purchased in 2009 or later (with a potential requirement to repay in full if requirements aren't met).

Step 2: Calculate the Repayment Based on Time Owned

Repayment is typically prorated based on how long you lived in the home before selling or changing residences.

Required ownership period: 36 months from date of purchase.

For every full month you fulfill the ownership requirement, you reduce what you owe by 1/36th.

For example:

Original Credit: $7,500

Months Owned: 18

Repayment = (36 - 18) / 36 = 50% of credit = $3,750

Step 3: Apply Any Applicable Exceptions

There are a few IRS-sanctioned exceptions to repayment:

The home was destroyed or condemned (e.g., by fire or natural disaster).

You died during the repayment period — no further repayments are due.

Divorce or legal separation resulting in the transfer of ownership.

You’ll need to document these exceptions, typically with legal or insurance paperwork.

Filing Form 5405: A Step-by-Step Guide

Whether you manage your own taxes or outsource your filings, knowing what to expect on Form 5405 helps reduce errors and delays.

Major Sections of Form 5405

Part I – Used to notify the IRS that you ceased using the home as your main residence.

Part II – Required if you sold the home and need to calculate repayment.

Part III – Used for exceptions or other specific events requiring disclosure.

Filing Tips

Attach Form 5405 to your annual Form 1040 tax return.

Include payment on Schedule 2 (Additional Taxes) if repayment applies.

Clearly report the sale date, credit received, and documentation of exceptions (if applicable).

Use bookkeeping platforms or document vaults to retain escrow statements, tax returns, proof of residence, and IRS letters.

Can You Avoid Repayment of the First-Time Homebuyer Credit?

Yes — under certain conditions, taxpayers can avoid repayment altogether. That’s good news if any of the following apply to your situation.

Common Exceptions That Waive Repayment

You converted the home to a rental after the 36-month period.

You transferred the home to a spouse or ex-spouse under a divorce agreement.

The home was destroyed or condemned, and you didn’t acquire a replacement residence within two years.

The taxpayer died before completing repayment (in which case, no further action is needed).

Documentation is essential. File any applicable statements with your return and maintain these records in case of IRS inquiry.

You can verify exception qualifications on the official IRS Form 5405 publication and instructions.

Common Mistakes To Avoid

With your time split between company growth and compliance details, mistakes can slip through. Here are the most common missteps related to Form 5405:

Mistake | Remedy |

Forgetting to file Form 5405 | Annually review changes in residence if you claimed the credit. |

Reporting incorrect ownership data | Cross-reference closing documents and utility bills. |

Filing late or omitting the form | File with your 1040 annually if required—IRS penalties can apply. |

Missed exceptions | Review IRS criteria or speak with a tax advisor before filing. |

What Comes Next? Actionable Steps for Startup Operators

Here’s what founders should do now to stay ahead of repayment:

Audit your own tax history – Confirm if you've ever claimed the First-Time Homebuyer Credit.

Review home sale or relocation dates – Match them against the 36-month rule.

Run the Form 5405 calculation if repayment is due, and identify any potential exceptions.

Work with a tax professional or use founder-focused platforms to automate this as part of your finance process.

If you’re relying on personal liquidity or creditworthiness to support your startup, compliant and transparent tax records keep you ready for your next raise, audit, or investment round.

Mastering Form 5405 Is About Protecting Your Startup’s Future

Form 5405 plays a critical role in calculating and reporting repayment of the First-Time Homebuyer Credit. If you’ve sold your home or changed residences after claiming this credit, understanding your filing obligations prevents costly surprises from disrupting your personal or business finances.

This article was co-written by:

Content

This article was co-written by:

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.