Go Back

Last Updated :

Last Updated :

Nov 13, 2025

Nov 13, 2025

Bookkeeping for Doctors: Manage Practice Finances With Confidence

Running a medical practice is a complex endeavor that demands your time and expertise in patient care. Yet, the financial side of your practice — from tracking expenses to managing revenue cycles — requires just as much attention to ensure your business thrives. Bookkeeping for doctors is a vital element that can be overlooked, but mastering it allows you to steer your practice with confidence and clarity.

This article offers practical guidance tailored specifically for medical professionals who want to gain control over finances without being buried in accounting jargon or administrative overload.

Whether you’re just starting a private practice, running a small group, or managing an established clinic, these insights will help streamline your financial management and free you up to focus on patient care.

Why Bookkeeping for Doctors is Different — And Why It Matters

Medical practices have unique financial dynamics that separate them from most other small businesses. You’re managing insurance reimbursements, patient copays, medical supplies expenses, staff payroll, compliance with healthcare regulations, and possibly multiple revenue streams such as direct patient billing, Medicare, Medicaid, and private insurers.

These complexities mean your bookkeeping process isn’t just about entering receipts and invoices; it requires specific attention to:

Accurate revenue tracking segmented by insurance type and payment status

Expense categorization for deductible medical supplies and equipment

Payroll management for clinical and administrative staff

Compliance with tax and healthcare regulations unique to medical providers

When done well, precise bookkeeping enables you to:

Identify cash flow patterns and anticipate gaps

Optimize your revenue cycle management (RCM) efficiency

Prepare for tax season without last-minute surprises

Make informed decisions about budgeting and investing in your practice’s growth

Without a customized bookkeeping approach, you risk financial inaccuracies, delayed collections, and missed tax benefits, all of which can impact your practice’s sustainability.

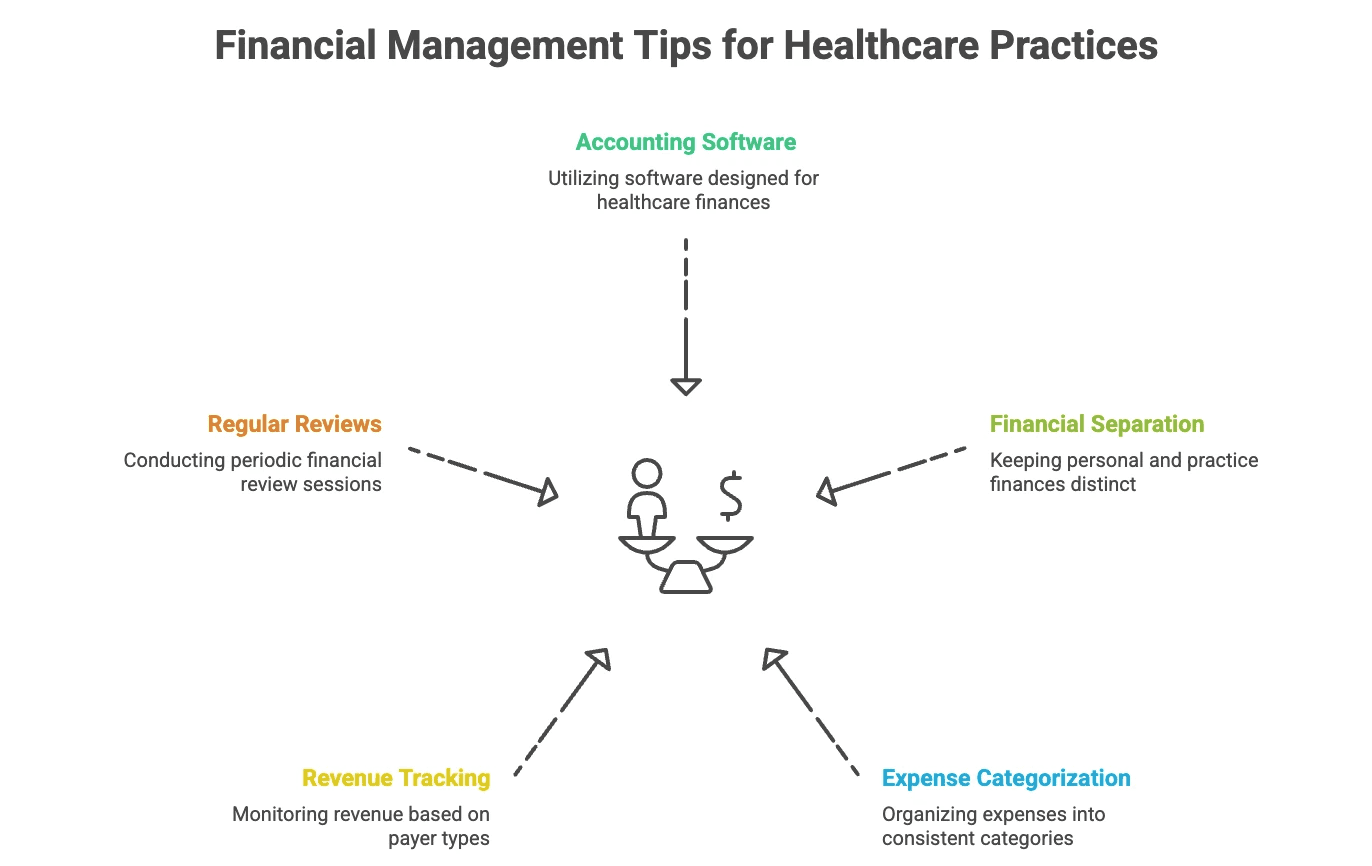

Bookkeeping for Medical Practices: Key Tips

Mastering bookkeeping for doctors comes down to several best practices that align with the operational realities of healthcare businesses. Below are actionable steps you can adopt to make your financial processes more efficient and insightful.

Use Specialized Accounting Software Tailored to Healthcare

General bookkeeping software often lacks the functionality to manage complex healthcare billing workflows. Consider platforms that integrate with your electronic health record (EHR) system and support insurance claim tracking. Features to prioritize include:

Patient billing and payment tracking

Insurance claim submission and follow-up

Automated reconciliation between payments received and invoices issued

Custom or integration-capable solutions reduce manual entry errors and accelerate revenue collection. For instance, modern bookkeeping services like Haven’s are designed with startups and healthcare firms in mind to streamline these workflows.

Separate Personal and Practice Finances

Many founders unknowingly mix personal and business expenses, which complicates tax reporting and weakens your understanding of the practice’s true financial position. Establish dedicated bank accounts and credit cards solely for your practice. This separation is also effective in simplifying your bookkeeping by making expenses easier to categorize.

Maintain Consistent Expense Categorization and Documentation

The IRS has specific rules about what medical practice expenses can be deducted. Common deductible costs include medical supplies, office rent, equipment depreciation, and staff salaries. Keep clear digital or physical records, including receipts and invoices, properly categorized (e.g., rent vs. supplies). This documentation will be invaluable during tax preparation and audit reviews.

Track Revenue by Payer Type

Insurance reimbursements can be delayed or denied, while direct patient payments may be immediate but variable. Use bookkeeping practices that allow you to tag revenue by payer source — Medicare, Medicaid, private insurance, and self-pay patients. This enables you to monitor which revenue streams are slow-paying or underperforming, allowing targeted follow-up action.

Schedule Regular Financial Review Sessions

Weekly or biweekly review meetings focused on bookkeeping reports can catch errors early, identify operational bottlenecks, and keep your practice’s financial health top of mind. Your review checklist might include:

Outstanding patient balances and aged receivables

Expense trends and cost control opportunities

Payroll and tax filing deadlines

These sessions encourage accountability and inform strategic decisions about staffing, marketing, or capital expenditures.

Managing Taxes and Compliance for Medical Practices

Beyond day-to-day bookkeeping, medical practices face tax complexity, including quarterly estimated payments, payroll tax withholding, and compliance with HIPAA and IRS legal requirements. Here are practical considerations to keep your practice tax-compliant and financially optimized.

Tax Element | Description | Founder Actionable Tips |

Quarterly Estimated Taxes | Practice owners must estimate and pay taxes on income four times a year. | Work with your finance lead or a bookkeeping partner to forecast taxable income and avoid penalties. |

Payroll Taxes | Includes Social Security, Medicare, and unemployment insurance taxes. | Automate payroll or use a trusted service to ensure accuracy and timeliness. |

Deductible Medical Expenses | Includes office rent, supplies, continuing education, and equipment depreciation. | Track meticulously throughout the year for tax optimization. |

ACA Compliance Reporting | Reporting on employee health coverage if you meet certain size thresholds. | Ensure payroll and bookkeeping data align to complete IRS forms accurately. |

Engaging a professional service like Haven’s tax filing and advisory services helps prevent costly mistakes and uncovers eligible tax credits, such as the R&D tax credit if your practice invests in developing new medical procedures or software.

For an authoritative overview of tax filing requirements, visit the IRS’s Small Business and Self-Employed Tax Center.

How Modern Bookkeeping Services Can Support Your Practice

Many doctors prefer to focus solely on patient care instead of wrestling with bookkeeping. Outsourcing your bookkeeping to a specialized partner can yield numerous benefits:

Responsive support tailored for founders

Dynamic startups and growing practices need fast answers and proactive advice. Look for bookkeeping providers attentive to your schedule and business growth needs.

Scalable processes as your practice expands

Cloud-based bookkeeping solutions adapt to more patients, providers, and complex revenue cycles without disruption.

Integrated services

Full-service offerings include bookkeeping, tax filing, payroll processing, and R&D tax credit support, allowing simplified vendor management.

Transparent reports

Clean, easy-to-understand financial statements allow you to grasp the financial health of your practice quickly and confidently.

Confident Financial Control with Expert Bookkeeping for Doctors

Mastering bookkeeping for doctors is not just about compliance; it’s a strategic advantage that enhances your practice’s sustainability and growth. By adopting tailored bookkeeping systems, maintaining clear financial boundaries, and regularly reviewing your financial health, you will gain clarity and control over your business.

With the complexity of insurance reimbursements, regulatory compliance, and tax reporting, partnering with modern bookkeeping experts like Haven provides you the freedom to prioritize patient care while ensuring your practice’s financial foundation is solid.

Running a medical practice is a complex endeavor that demands your time and expertise in patient care. Yet, the financial side of your practice — from tracking expenses to managing revenue cycles — requires just as much attention to ensure your business thrives. Bookkeeping for doctors is a vital element that can be overlooked, but mastering it allows you to steer your practice with confidence and clarity.

This article offers practical guidance tailored specifically for medical professionals who want to gain control over finances without being buried in accounting jargon or administrative overload.

Whether you’re just starting a private practice, running a small group, or managing an established clinic, these insights will help streamline your financial management and free you up to focus on patient care.

Why Bookkeeping for Doctors is Different — And Why It Matters

Medical practices have unique financial dynamics that separate them from most other small businesses. You’re managing insurance reimbursements, patient copays, medical supplies expenses, staff payroll, compliance with healthcare regulations, and possibly multiple revenue streams such as direct patient billing, Medicare, Medicaid, and private insurers.

These complexities mean your bookkeeping process isn’t just about entering receipts and invoices; it requires specific attention to:

Accurate revenue tracking segmented by insurance type and payment status

Expense categorization for deductible medical supplies and equipment

Payroll management for clinical and administrative staff

Compliance with tax and healthcare regulations unique to medical providers

When done well, precise bookkeeping enables you to:

Identify cash flow patterns and anticipate gaps

Optimize your revenue cycle management (RCM) efficiency

Prepare for tax season without last-minute surprises

Make informed decisions about budgeting and investing in your practice’s growth

Without a customized bookkeeping approach, you risk financial inaccuracies, delayed collections, and missed tax benefits, all of which can impact your practice’s sustainability.

Bookkeeping for Medical Practices: Key Tips

Mastering bookkeeping for doctors comes down to several best practices that align with the operational realities of healthcare businesses. Below are actionable steps you can adopt to make your financial processes more efficient and insightful.

Use Specialized Accounting Software Tailored to Healthcare

General bookkeeping software often lacks the functionality to manage complex healthcare billing workflows. Consider platforms that integrate with your electronic health record (EHR) system and support insurance claim tracking. Features to prioritize include:

Patient billing and payment tracking

Insurance claim submission and follow-up

Automated reconciliation between payments received and invoices issued

Custom or integration-capable solutions reduce manual entry errors and accelerate revenue collection. For instance, modern bookkeeping services like Haven’s are designed with startups and healthcare firms in mind to streamline these workflows.

Separate Personal and Practice Finances

Many founders unknowingly mix personal and business expenses, which complicates tax reporting and weakens your understanding of the practice’s true financial position. Establish dedicated bank accounts and credit cards solely for your practice. This separation is also effective in simplifying your bookkeeping by making expenses easier to categorize.

Maintain Consistent Expense Categorization and Documentation

The IRS has specific rules about what medical practice expenses can be deducted. Common deductible costs include medical supplies, office rent, equipment depreciation, and staff salaries. Keep clear digital or physical records, including receipts and invoices, properly categorized (e.g., rent vs. supplies). This documentation will be invaluable during tax preparation and audit reviews.

Track Revenue by Payer Type

Insurance reimbursements can be delayed or denied, while direct patient payments may be immediate but variable. Use bookkeeping practices that allow you to tag revenue by payer source — Medicare, Medicaid, private insurance, and self-pay patients. This enables you to monitor which revenue streams are slow-paying or underperforming, allowing targeted follow-up action.

Schedule Regular Financial Review Sessions

Weekly or biweekly review meetings focused on bookkeeping reports can catch errors early, identify operational bottlenecks, and keep your practice’s financial health top of mind. Your review checklist might include:

Outstanding patient balances and aged receivables

Expense trends and cost control opportunities

Payroll and tax filing deadlines

These sessions encourage accountability and inform strategic decisions about staffing, marketing, or capital expenditures.

Managing Taxes and Compliance for Medical Practices

Beyond day-to-day bookkeeping, medical practices face tax complexity, including quarterly estimated payments, payroll tax withholding, and compliance with HIPAA and IRS legal requirements. Here are practical considerations to keep your practice tax-compliant and financially optimized.

Tax Element | Description | Founder Actionable Tips |

Quarterly Estimated Taxes | Practice owners must estimate and pay taxes on income four times a year. | Work with your finance lead or a bookkeeping partner to forecast taxable income and avoid penalties. |

Payroll Taxes | Includes Social Security, Medicare, and unemployment insurance taxes. | Automate payroll or use a trusted service to ensure accuracy and timeliness. |

Deductible Medical Expenses | Includes office rent, supplies, continuing education, and equipment depreciation. | Track meticulously throughout the year for tax optimization. |

ACA Compliance Reporting | Reporting on employee health coverage if you meet certain size thresholds. | Ensure payroll and bookkeeping data align to complete IRS forms accurately. |

Engaging a professional service like Haven’s tax filing and advisory services helps prevent costly mistakes and uncovers eligible tax credits, such as the R&D tax credit if your practice invests in developing new medical procedures or software.

For an authoritative overview of tax filing requirements, visit the IRS’s Small Business and Self-Employed Tax Center.

How Modern Bookkeeping Services Can Support Your Practice

Many doctors prefer to focus solely on patient care instead of wrestling with bookkeeping. Outsourcing your bookkeeping to a specialized partner can yield numerous benefits:

Responsive support tailored for founders

Dynamic startups and growing practices need fast answers and proactive advice. Look for bookkeeping providers attentive to your schedule and business growth needs.

Scalable processes as your practice expands

Cloud-based bookkeeping solutions adapt to more patients, providers, and complex revenue cycles without disruption.

Integrated services

Full-service offerings include bookkeeping, tax filing, payroll processing, and R&D tax credit support, allowing simplified vendor management.

Transparent reports

Clean, easy-to-understand financial statements allow you to grasp the financial health of your practice quickly and confidently.

Confident Financial Control with Expert Bookkeeping for Doctors

Mastering bookkeeping for doctors is not just about compliance; it’s a strategic advantage that enhances your practice’s sustainability and growth. By adopting tailored bookkeeping systems, maintaining clear financial boundaries, and regularly reviewing your financial health, you will gain clarity and control over your business.

With the complexity of insurance reimbursements, regulatory compliance, and tax reporting, partnering with modern bookkeeping experts like Haven provides you the freedom to prioritize patient care while ensuring your practice’s financial foundation is solid.

This article was co-written by:

Content

This article was co-written by:

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.