Go Back

Last Updated :

Last Updated :

Nov 7, 2025

Nov 7, 2025

Smart Tax Planning Strategies for Small Businesses

Running a small business means juggling many moving parts — customers, employees, operations, and finances. One of the biggest challenges for business owners is managing taxes effectively. When tax season arrives, small businesses face higher stakes than individuals: complex filings, changing regulations, and the risk of missing valuable deductions.

Smart small business tax planning strategies help you minimize liabilities, maximize deductions, and reduce stress. This guide covers key tax planning principles, commonly overlooked tax deductions for small businesses, and ways to strengthen your year-round approach to compliance and savings.

Understanding Small Business Taxes

Every small business has unique tax responsibilities. Understanding which taxes apply to you — and how to prepare for them — is the first step in effective planning.

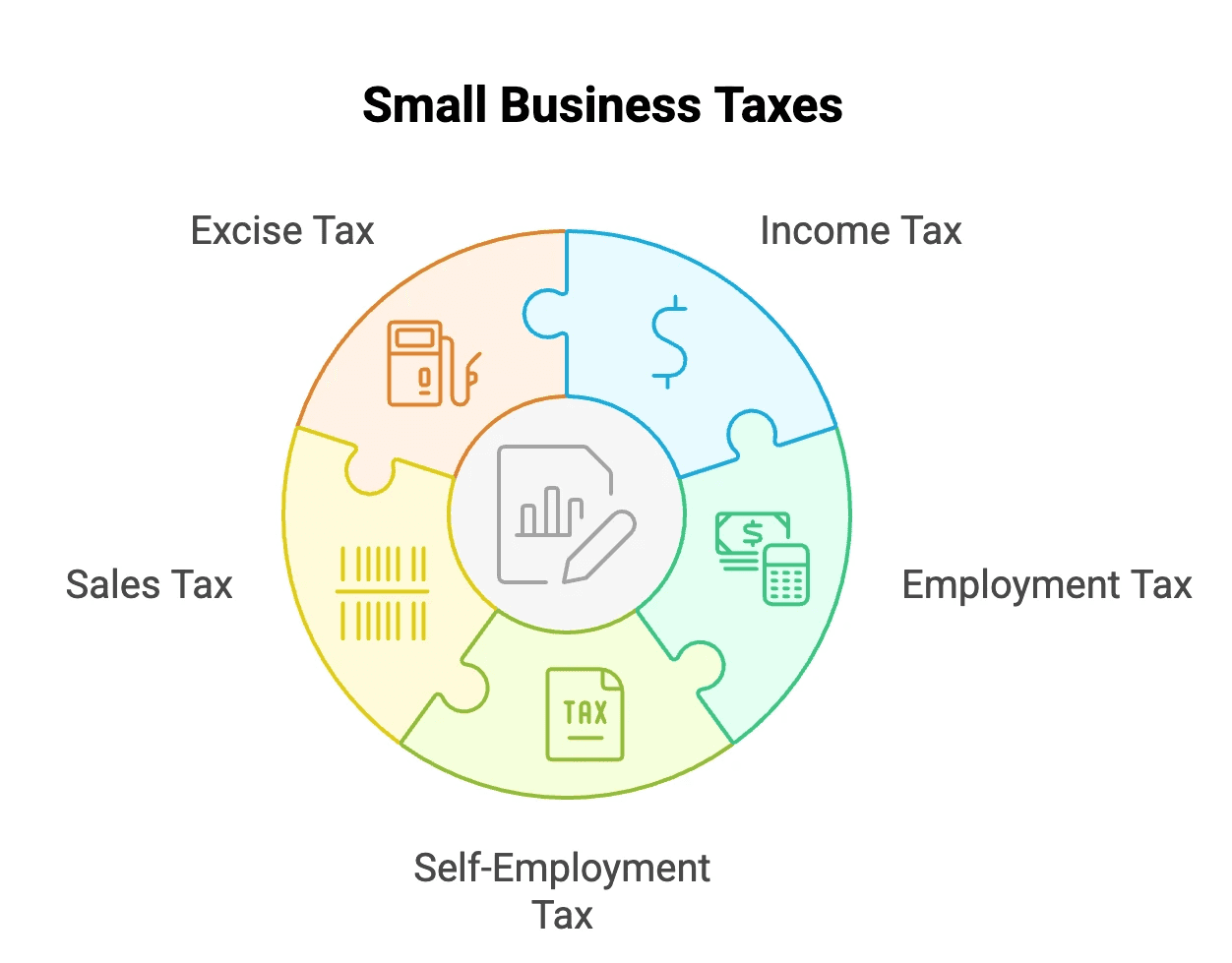

Types of Small Business Taxes

Most small businesses pay a mix of the following:

Income Tax: All businesses (except partnerships, which pass income through to owners) must file a federal income tax return each year.

Employment Tax: Businesses with employees must pay employment taxes, including Social Security, Medicare, and Federal Unemployment Tax (FUTA).

Self-Employment Tax: Sole proprietors and partners pay self-employment tax to cover Social Security and Medicare.

Sales Tax: Businesses may need to collect and remit sales taxes to state or local authorities.

Excise Tax: Applies to certain industries or products, such as fuel or environmental services.

Tax Forms and Filing Requirements by Business Entity Type

Understanding which forms to file — and how — helps ensure compliance and avoid costly mistakes. The table below summarizes federal filing requirements for common business structures.

Federal tax filing requirements by business entity type:

Business Entity Type | Federal Income Tax Form | Notes on Filing |

Sole Proprietorship | Schedule C (Form 1040) | Income and expenses reported on personal tax return. |

Single-Member LLC | Schedule C (Form 1040) | Treated as a sole proprietorship for tax purposes; reported on personal return. |

Partnership | Form 1065 | Information return only; partners receive K-1s for personal returns. |

Multi-Member LLC | Form 1065 | Treated as a partnership for tax purposes; reported on personal returns via K-1s. |

S Corporation | Form 1120S | Separate corporate return; income/losses pass through to owners via K-1s. |

C Corporation | Form 1120 | Separate corporate return; pays corporate income tax directly. |

4 Effective Tax Planning Strategies for Small Businesses

Strong tax planning strategies for small businesses can reduce your tax bill and help you reinvest savings into growth. To make these easier to navigate, we’ve grouped them into four key categories:

Deduction & Credit Optimization

Maximize Qualified Deductions: Track every legitimate business expense — from office supplies to marketing costs — to claim all available deductions.

Leverage Small Business Tax Credits: Explore credits like the R&D Tax Credit or Small Employer Health Insurance Premium Credit to offset liability.

Carry Forward Unused Deductions: Use net operating losses (NOLs) or capital losses to reduce future taxable income.

Structural & Strategic Adjustments

Review Your Business Entity Type: The right structure (LLC, S Corp, C Corp) affects your tax exposure and filing complexity.

Adopt or Contribute to a Qualified Retirement Plan: Contributions can lower taxable income while supporting long-term financial goals.

Use an Accountable Plan: Properly document and reimburse employee expenses for travel, home office, or equipment.

Defer Income Strategically: Shift income or expenses between years to align with expected profits and tax brackets.

Operational Efficiency

Hire a CPA for Small Business: A qualified CPA helps identify missed opportunities and ensures compliance — especially for complex deductions or multi-state operations.

Maintain Accurate Recordkeeping: Reliable books make it easier to claim legitimate deductions and defend your position if audited.

Invest in New Assets Before Year-End: Purchasing equipment before December 31 can qualify you for immediate or bonus depreciation.

Offer Employee Benefits: Contributions to health insurance or retirement plans are deductible and improve team retention.

Specialized Planning Opportunities

Deduct Startup and Organizational Costs: New businesses can deduct up to $5,000 in startup and $5,000 in organizational costs.

Claim the Home Office Deduction: Deduct a portion of utilities, insurance, and maintenance if your workspace meets IRS “exclusive use” standards.

Handle Bad Debt Correctly: Write off income that won’t be collected once it’s proven uncollectible.

Deduct Marketing & Professional Fees: Costs for advertising, web design, or outsourced accounting are fully deductible.

Commonly Overlooked Tax Deductions for Small Businesses

Many business owners miss simple deductions that can meaningfully lower their tax bill, such as:

Business insurance premiums

Software subscriptions and accounting tools

Continuing education or industry training

Banking and payment processing fees

Mileage for business-related travel

Staying proactive with documentation ensures these legitimate costs are recognized at filing time.

Benefits of Working with a CPA or Tax Advisor

Even when your goal is to manage finances in-house, collaborating with a CPA for small business brings measurable value. A professional helps you:

Identify all eligible deductions and credits

Avoid filing errors that trigger audits

Stay up to date on annual IRS changes

Save time — the IRS estimates it takes an average of 13 hours to self-file

Build long-term confidence in your financial records

Partnering with a trusted advisor isn’t just about compliance — it’s about optimizing your resources year-round.

How Haven Supports Your Small Business Tax Planning

At Haven, we work alongside founders and finance leads to simplify complex tax and accounting tasks. Our team helps small businesses and startups manage:

Tax Filings & Credits: Accurate filings and R&D credit optimization to reduce liabilities.

Bookkeeping & Financial Visibility: Clean, board-ready financials for confident decision-making.

Fractional CFO Insights: Strategic guidance that connects tax planning to your growth goals.

Haven supports 400+ growing companies in managing their books, filings, and credits seamlessly — so you can focus on scaling your business, not your paperwork.

Key Takeaway

Effective small business tax planning isn’t just about surviving tax season — it’s about building a strategy that supports long-term growth. Whether you manage filings internally or partner with experts, staying proactive and informed helps you protect your profits and peace of mind.

Frequently Asked Questions About Small Business Tax Planning

What tax forms do small businesses file?

It depends on your structure. Sole proprietors and single-member LLCs use Schedule C (Form 1040); partnerships use Form 1065; S Corporations file Form 1120S; C Corporations file Form 1120.

How can I reduce my small business tax liability?

Focus on deductions, tax credits, and expense tracking. Consider contributing to retirement plans, deferring income strategically, or hiring a CPA for small business guidance.

Are home office expenses deductible?

Yes — if the space is used regularly and exclusively for business, per IRS Publication 587.

Why work with a CPA instead of filing taxes yourself?

A CPA provides expertise, accuracy, and ongoing compliance support. This often saves both time and money by preventing errors and missed opportunities.

Running a small business means juggling many moving parts — customers, employees, operations, and finances. One of the biggest challenges for business owners is managing taxes effectively. When tax season arrives, small businesses face higher stakes than individuals: complex filings, changing regulations, and the risk of missing valuable deductions.

Smart small business tax planning strategies help you minimize liabilities, maximize deductions, and reduce stress. This guide covers key tax planning principles, commonly overlooked tax deductions for small businesses, and ways to strengthen your year-round approach to compliance and savings.

Understanding Small Business Taxes

Every small business has unique tax responsibilities. Understanding which taxes apply to you — and how to prepare for them — is the first step in effective planning.

Types of Small Business Taxes

Most small businesses pay a mix of the following:

Income Tax: All businesses (except partnerships, which pass income through to owners) must file a federal income tax return each year.

Employment Tax: Businesses with employees must pay employment taxes, including Social Security, Medicare, and Federal Unemployment Tax (FUTA).

Self-Employment Tax: Sole proprietors and partners pay self-employment tax to cover Social Security and Medicare.

Sales Tax: Businesses may need to collect and remit sales taxes to state or local authorities.

Excise Tax: Applies to certain industries or products, such as fuel or environmental services.

Tax Forms and Filing Requirements by Business Entity Type

Understanding which forms to file — and how — helps ensure compliance and avoid costly mistakes. The table below summarizes federal filing requirements for common business structures.

Federal tax filing requirements by business entity type:

Business Entity Type | Federal Income Tax Form | Notes on Filing |

Sole Proprietorship | Schedule C (Form 1040) | Income and expenses reported on personal tax return. |

Single-Member LLC | Schedule C (Form 1040) | Treated as a sole proprietorship for tax purposes; reported on personal return. |

Partnership | Form 1065 | Information return only; partners receive K-1s for personal returns. |

Multi-Member LLC | Form 1065 | Treated as a partnership for tax purposes; reported on personal returns via K-1s. |

S Corporation | Form 1120S | Separate corporate return; income/losses pass through to owners via K-1s. |

C Corporation | Form 1120 | Separate corporate return; pays corporate income tax directly. |

4 Effective Tax Planning Strategies for Small Businesses

Strong tax planning strategies for small businesses can reduce your tax bill and help you reinvest savings into growth. To make these easier to navigate, we’ve grouped them into four key categories:

Deduction & Credit Optimization

Maximize Qualified Deductions: Track every legitimate business expense — from office supplies to marketing costs — to claim all available deductions.

Leverage Small Business Tax Credits: Explore credits like the R&D Tax Credit or Small Employer Health Insurance Premium Credit to offset liability.

Carry Forward Unused Deductions: Use net operating losses (NOLs) or capital losses to reduce future taxable income.

Structural & Strategic Adjustments

Review Your Business Entity Type: The right structure (LLC, S Corp, C Corp) affects your tax exposure and filing complexity.

Adopt or Contribute to a Qualified Retirement Plan: Contributions can lower taxable income while supporting long-term financial goals.

Use an Accountable Plan: Properly document and reimburse employee expenses for travel, home office, or equipment.

Defer Income Strategically: Shift income or expenses between years to align with expected profits and tax brackets.

Operational Efficiency

Hire a CPA for Small Business: A qualified CPA helps identify missed opportunities and ensures compliance — especially for complex deductions or multi-state operations.

Maintain Accurate Recordkeeping: Reliable books make it easier to claim legitimate deductions and defend your position if audited.

Invest in New Assets Before Year-End: Purchasing equipment before December 31 can qualify you for immediate or bonus depreciation.

Offer Employee Benefits: Contributions to health insurance or retirement plans are deductible and improve team retention.

Specialized Planning Opportunities

Deduct Startup and Organizational Costs: New businesses can deduct up to $5,000 in startup and $5,000 in organizational costs.

Claim the Home Office Deduction: Deduct a portion of utilities, insurance, and maintenance if your workspace meets IRS “exclusive use” standards.

Handle Bad Debt Correctly: Write off income that won’t be collected once it’s proven uncollectible.

Deduct Marketing & Professional Fees: Costs for advertising, web design, or outsourced accounting are fully deductible.

Commonly Overlooked Tax Deductions for Small Businesses

Many business owners miss simple deductions that can meaningfully lower their tax bill, such as:

Business insurance premiums

Software subscriptions and accounting tools

Continuing education or industry training

Banking and payment processing fees

Mileage for business-related travel

Staying proactive with documentation ensures these legitimate costs are recognized at filing time.

Benefits of Working with a CPA or Tax Advisor

Even when your goal is to manage finances in-house, collaborating with a CPA for small business brings measurable value. A professional helps you:

Identify all eligible deductions and credits

Avoid filing errors that trigger audits

Stay up to date on annual IRS changes

Save time — the IRS estimates it takes an average of 13 hours to self-file

Build long-term confidence in your financial records

Partnering with a trusted advisor isn’t just about compliance — it’s about optimizing your resources year-round.

How Haven Supports Your Small Business Tax Planning

At Haven, we work alongside founders and finance leads to simplify complex tax and accounting tasks. Our team helps small businesses and startups manage:

Tax Filings & Credits: Accurate filings and R&D credit optimization to reduce liabilities.

Bookkeeping & Financial Visibility: Clean, board-ready financials for confident decision-making.

Fractional CFO Insights: Strategic guidance that connects tax planning to your growth goals.

Haven supports 400+ growing companies in managing their books, filings, and credits seamlessly — so you can focus on scaling your business, not your paperwork.

Key Takeaway

Effective small business tax planning isn’t just about surviving tax season — it’s about building a strategy that supports long-term growth. Whether you manage filings internally or partner with experts, staying proactive and informed helps you protect your profits and peace of mind.

Frequently Asked Questions About Small Business Tax Planning

What tax forms do small businesses file?

It depends on your structure. Sole proprietors and single-member LLCs use Schedule C (Form 1040); partnerships use Form 1065; S Corporations file Form 1120S; C Corporations file Form 1120.

How can I reduce my small business tax liability?

Focus on deductions, tax credits, and expense tracking. Consider contributing to retirement plans, deferring income strategically, or hiring a CPA for small business guidance.

Are home office expenses deductible?

Yes — if the space is used regularly and exclusively for business, per IRS Publication 587.

Why work with a CPA instead of filing taxes yourself?

A CPA provides expertise, accuracy, and ongoing compliance support. This often saves both time and money by preventing errors and missed opportunities.

This article was co-written by:

Content

This article was co-written by:

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.