Go Back

Last Updated :

Last Updated :

Nov 7, 2025

Nov 7, 2025

Are Business Loan Payments Tax Deductible? A Founder’s Guide to Getting It Right

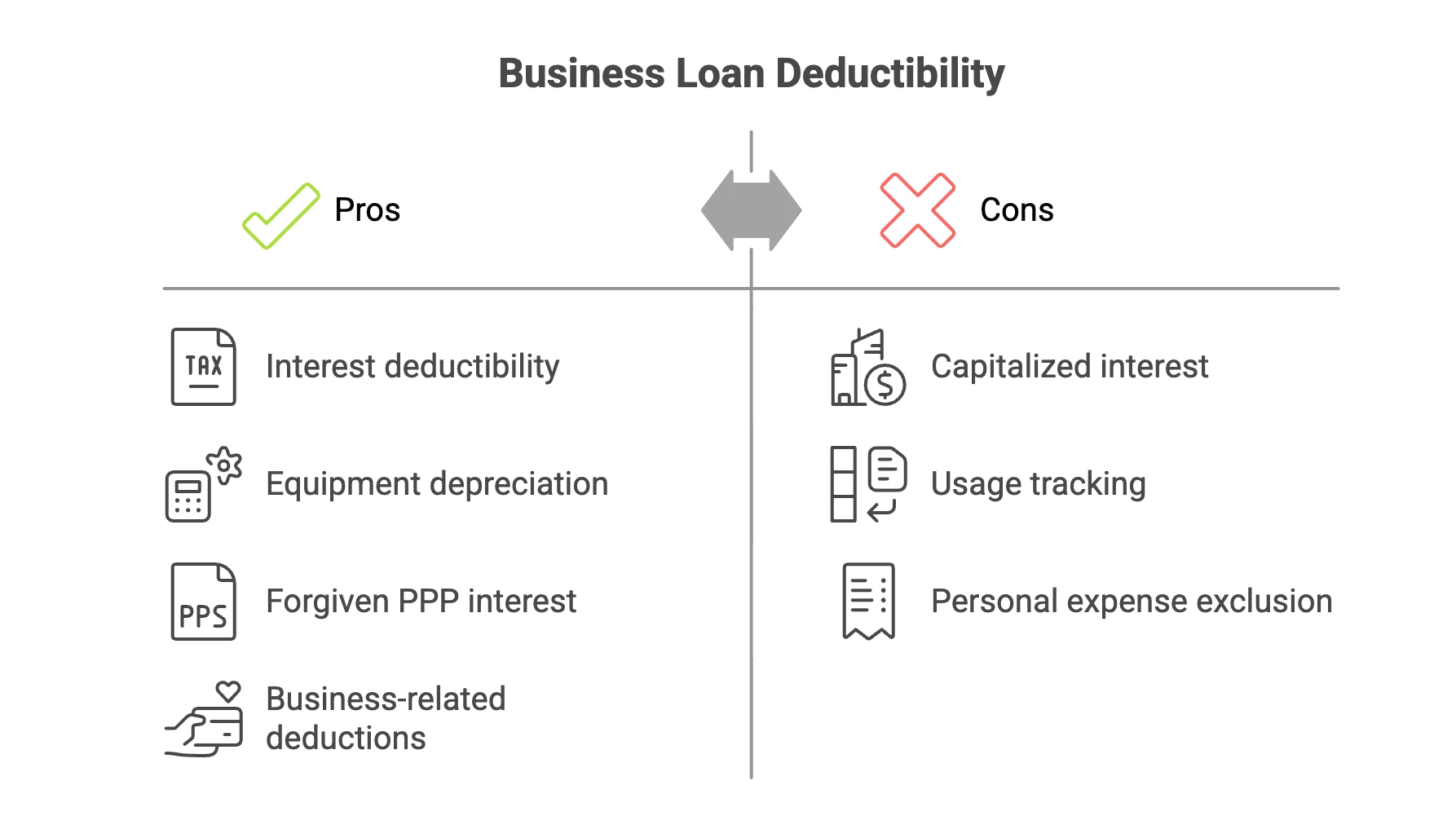

Business loans keep your company moving, from covering payroll to funding new launches. But when tax season hits, every founder asks: Are business loan payments tax-deductible?

The short answer: not all of them.

Only certain parts of each payment qualify. Knowing the difference helps you stay compliant, reduce tax liability, and make smarter financing decisions.

Principal vs. Interest: What’s Actually Deductible

Each payment includes principal and interest, and the IRS treats them differently.

Principal: The money you borrowed. Paying it back isn’t deductible — you’re just returning borrowed funds.

Interest: The cost of borrowing. It’s deductible when the loan is used for business purposes.

Example: If you pay $1,200 per month and $840 goes toward principal while $360 is interest, you can only deduct the $360.

Pro tip: Keep your lender’s amortization schedule handy. It separates principal and interest, helping your CPA record deductions accurately and avoid missed write-offs.

Who Can Deduct Business Loan Interest

To qualify for a business loan interest deduction, two things must be true:

You’re legally liable for the loan — it’s in your name or your business’s name.

You used the funds for business purposes.

If part of a personal loan funded your business, you can still deduct the business-use percentage of the interest.

Example: If 70% of a loan funded equipment and 30% was personal, only 70% of the interest qualifies.

Keep receipts, transfers, and invoices that prove business use — the IRS looks for this documentation during audits.

Cash vs. Accrual Accounting: When to Take the Deduction

This table breaks down when startups can deduct loan interest depending on their accounting method.

Under the cash basis, you record the deduction once the interest is actually paid — supported by proof like bank statements or receipts.

The accrual basis recognizes the expense as soon as the interest is incurred, requiring more detailed records such as accrual entries and reconciliations.

Accounting Method | When You Deduct | Records Needed |

Cash Basis | When interest is paid | Bank statements, proof of payment |

Accrual Basis | When interest is incurred | Accrual entries, reconciliations |

Most early-stage startups use cash basis — you deduct interest when it’s paid. Accrual-basis companies can deduct as it accrues.

Consistency is key. Use your chosen method across all filings to keep your books audit-ready.

Need a broader cash plan? See our guide to 10 Ways to Save Money on Business Taxes

Loan Fees, Points & Penalties: The Hidden Costs

Business loans come with extra charges that affect deductibility:

Origination Fees / Points: Usually capitalized and deducted over the loan’s life.

Prepayment Penalties: Deductible when paid — considered additional interest.

Late Fees: Deductible if tied to business borrowing.

Ask your lender for an itemized breakdown to identify what can be deducted now versus later.

Section 163(j): The Business Interest Limitation Rule

The IRS section 163(j) may limit how much interest you can deduct in a year.

The Cap: Up to 30% of adjusted taxable income (ATI).

Small Business Exception: If your business averages under $30 million in annual gross receipts, you’re exempt.

Carry forward Option: Disallowed interest can be carried forward indefinitely.

Form Required: File Form 8990 if this rule applies.

Quick Checklist

Calculate ATI (income before interest, depreciation, and amortization).

Apply the 30% cap.

File Form 8990 if required.

Keep supporting calculations for at least three years.

Loan Types and Deductibility Rules

Each business loan type comes with its own deduction rules.

The table below outlines how interest deductibility works for common financing options — from SBA and equipment loans to business credit cards. Knowing which records to keep and how to allocate funds helps ensure your deductions hold up under IRS review.

Loan Type | Deductibility Summary | Key Notes |

SBA Loan | Interest is deductible when used for business | Treated as a standard loan |

Equipment Loan | Interest deductible; equipment depreciable | Combine interest + Section 179 |

Commercial Real Estate | Interest deductible; construction interest capitalized | Separate phases |

PPP (Forgiven) | Forgiven principal not taxable; interest still deductible | Confirm current IRS guidance |

Business LOC | Interest is deductible on drawn amounts | Track usage |

Refinanced Loan | Deductible if funds are business-related | Allocate carefully |

Business Credit Card | Deduct interest on business charges | Exclude personal expenses |

Related-Party or Below-Market Loans

If your business borrows from an owner or related entity, the IRS applies extra scrutiny.

To keep deductions valid:

Charge a market-rate interest.

Use a written agreement.

Record payments properly.

Without documentation, the IRS may reclassify your “loan” as equity — wiping out deductions.

Stay Audit-Ready with Clean Records

Keep these on file:

Signed loan agreements

Amortization schedules

Bank statements

Proof of business use

Filed tax forms (Schedule C, Form 1065, 1120, or 8990)

Good record-keeping prevents audit issues and simplifies tax preparation.

For deeper organization tips, see Bookkeeping for Startups: Complete Founder Guide

Tax Planning Strategies for Founders

Time payments to maximize deductions (cash-basis).

Align interest deductions with depreciation schedules.

Explore elections that expand the deductibility of real estate or manufacturing expenses.

Work with startup CPAs who understand SAFE notes, R&D credits, and early-stage structures.

How Haven Helps Founders Stay Tax-Smart

You don’t have time to parse IRS forms or interest schedules.

Haven’s CPA-led team manages bookkeeping, tax filings, payroll, and R&D credits — so you can claim every legitimate deduction without the guesswork.

400+ startups trust Haven for fast, founder-first support through Slack — no ticket queues, no delays.

“Stop spending hours reconciling interest payments. We’ll do it — so you can get back to building.”

— Haven Accounting Team

Don't Leave Money on the table

Every missed deduction or delayed filing chips away at your runway. Haven helps you stay ahead — automating compliance, maximizing credits, and ensuring your books work as hard as you do. Let’s make sure you keep every dollar you’ve earned.

Business loans keep your company moving, from covering payroll to funding new launches. But when tax season hits, every founder asks: Are business loan payments tax-deductible?

The short answer: not all of them.

Only certain parts of each payment qualify. Knowing the difference helps you stay compliant, reduce tax liability, and make smarter financing decisions.

Principal vs. Interest: What’s Actually Deductible

Each payment includes principal and interest, and the IRS treats them differently.

Principal: The money you borrowed. Paying it back isn’t deductible — you’re just returning borrowed funds.

Interest: The cost of borrowing. It’s deductible when the loan is used for business purposes.

Example: If you pay $1,200 per month and $840 goes toward principal while $360 is interest, you can only deduct the $360.

Pro tip: Keep your lender’s amortization schedule handy. It separates principal and interest, helping your CPA record deductions accurately and avoid missed write-offs.

Who Can Deduct Business Loan Interest

To qualify for a business loan interest deduction, two things must be true:

You’re legally liable for the loan — it’s in your name or your business’s name.

You used the funds for business purposes.

If part of a personal loan funded your business, you can still deduct the business-use percentage of the interest.

Example: If 70% of a loan funded equipment and 30% was personal, only 70% of the interest qualifies.

Keep receipts, transfers, and invoices that prove business use — the IRS looks for this documentation during audits.

Cash vs. Accrual Accounting: When to Take the Deduction

This table breaks down when startups can deduct loan interest depending on their accounting method.

Under the cash basis, you record the deduction once the interest is actually paid — supported by proof like bank statements or receipts.

The accrual basis recognizes the expense as soon as the interest is incurred, requiring more detailed records such as accrual entries and reconciliations.

Accounting Method | When You Deduct | Records Needed |

Cash Basis | When interest is paid | Bank statements, proof of payment |

Accrual Basis | When interest is incurred | Accrual entries, reconciliations |

Most early-stage startups use cash basis — you deduct interest when it’s paid. Accrual-basis companies can deduct as it accrues.

Consistency is key. Use your chosen method across all filings to keep your books audit-ready.

Need a broader cash plan? See our guide to 10 Ways to Save Money on Business Taxes

Loan Fees, Points & Penalties: The Hidden Costs

Business loans come with extra charges that affect deductibility:

Origination Fees / Points: Usually capitalized and deducted over the loan’s life.

Prepayment Penalties: Deductible when paid — considered additional interest.

Late Fees: Deductible if tied to business borrowing.

Ask your lender for an itemized breakdown to identify what can be deducted now versus later.

Section 163(j): The Business Interest Limitation Rule

The IRS section 163(j) may limit how much interest you can deduct in a year.

The Cap: Up to 30% of adjusted taxable income (ATI).

Small Business Exception: If your business averages under $30 million in annual gross receipts, you’re exempt.

Carry forward Option: Disallowed interest can be carried forward indefinitely.

Form Required: File Form 8990 if this rule applies.

Quick Checklist

Calculate ATI (income before interest, depreciation, and amortization).

Apply the 30% cap.

File Form 8990 if required.

Keep supporting calculations for at least three years.

Loan Types and Deductibility Rules

Each business loan type comes with its own deduction rules.

The table below outlines how interest deductibility works for common financing options — from SBA and equipment loans to business credit cards. Knowing which records to keep and how to allocate funds helps ensure your deductions hold up under IRS review.

Loan Type | Deductibility Summary | Key Notes |

SBA Loan | Interest is deductible when used for business | Treated as a standard loan |

Equipment Loan | Interest deductible; equipment depreciable | Combine interest + Section 179 |

Commercial Real Estate | Interest deductible; construction interest capitalized | Separate phases |

PPP (Forgiven) | Forgiven principal not taxable; interest still deductible | Confirm current IRS guidance |

Business LOC | Interest is deductible on drawn amounts | Track usage |

Refinanced Loan | Deductible if funds are business-related | Allocate carefully |

Business Credit Card | Deduct interest on business charges | Exclude personal expenses |

Related-Party or Below-Market Loans

If your business borrows from an owner or related entity, the IRS applies extra scrutiny.

To keep deductions valid:

Charge a market-rate interest.

Use a written agreement.

Record payments properly.

Without documentation, the IRS may reclassify your “loan” as equity — wiping out deductions.

Stay Audit-Ready with Clean Records

Keep these on file:

Signed loan agreements

Amortization schedules

Bank statements

Proof of business use

Filed tax forms (Schedule C, Form 1065, 1120, or 8990)

Good record-keeping prevents audit issues and simplifies tax preparation.

For deeper organization tips, see Bookkeeping for Startups: Complete Founder Guide

Tax Planning Strategies for Founders

Time payments to maximize deductions (cash-basis).

Align interest deductions with depreciation schedules.

Explore elections that expand the deductibility of real estate or manufacturing expenses.

Work with startup CPAs who understand SAFE notes, R&D credits, and early-stage structures.

How Haven Helps Founders Stay Tax-Smart

You don’t have time to parse IRS forms or interest schedules.

Haven’s CPA-led team manages bookkeeping, tax filings, payroll, and R&D credits — so you can claim every legitimate deduction without the guesswork.

400+ startups trust Haven for fast, founder-first support through Slack — no ticket queues, no delays.

“Stop spending hours reconciling interest payments. We’ll do it — so you can get back to building.”

— Haven Accounting Team

Don't Leave Money on the table

Every missed deduction or delayed filing chips away at your runway. Haven helps you stay ahead — automating compliance, maximizing credits, and ensuring your books work as hard as you do. Let’s make sure you keep every dollar you’ve earned.

This article was co-written by:

Content

This article was co-written by:

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.