Go Back

Last Updated :

Last Updated :

Nov 7, 2025

Nov 7, 2025

The Ultimate Guide to the R&D Tax Credit (2025 Update)

Innovation is expensive. The R&D Tax Credit exists to give that money back to founders building something new. The R&D Tax Credit helps startups reinvest in innovation rather than hand that money to the IRS.

In this guide, you’ll learn what the R&D Tax Credit is, who qualifies, how to calculate it, how to claim it properly, and how to avoid common misconceptions that cause companies to miss out on savings.

What Is the R&D Tax Credit?

The R&D Tax Credit is a government incentive designed to stimulate innovation and technological advancement. In the United States, it is administered by the Internal Revenue Service (IRS) and allows eligible businesses to claim a credit for a portion of their qualified research expenses (QREs).

These expenses may include the costs of developing new products, improving manufacturing processes, or experimenting with innovative technologies. The goal is to reduce the financial risk associated with R&D and help companies pursue projects that advance science, technology, and productivity.

Key purposes of the R&D Tax Credit:

Encourage companies to invest in research and innovation;

Stimulate economic growth and high-skilled employment;

Offset some of the costs and uncertainties associated with experimentation.

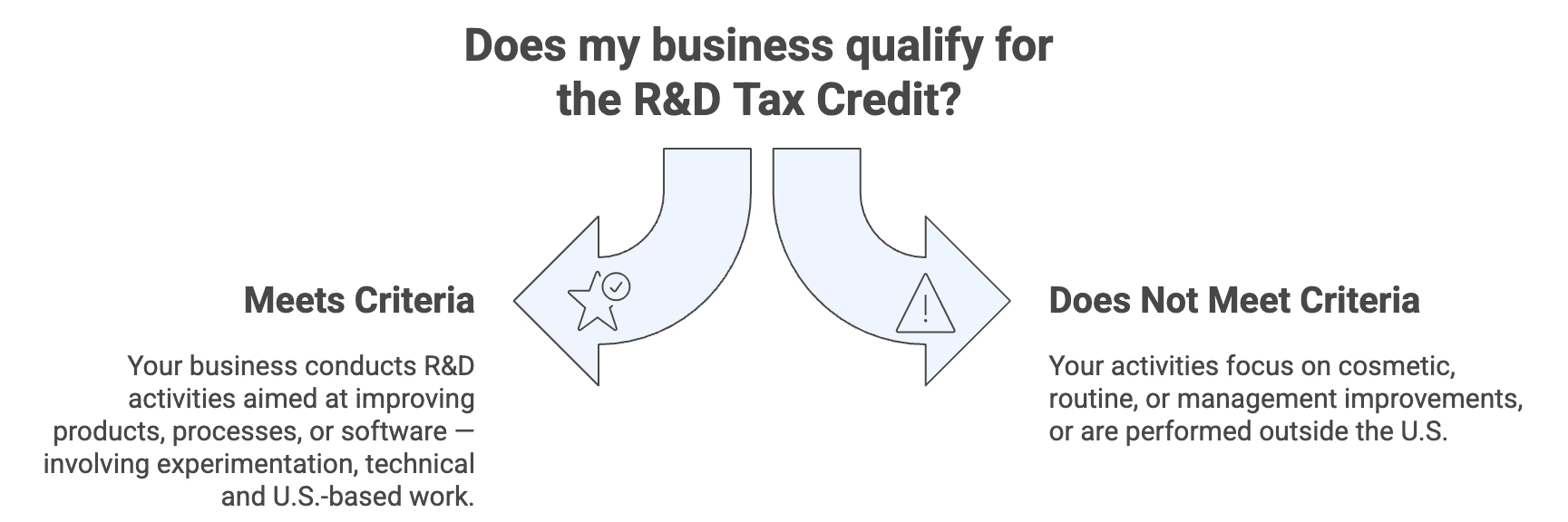

Eligibility Criteria for the R&D Tax Credit

To claim the R&D Tax Credit, your business must meet certain eligibility requirements defined by the IRS. Contrary to popular belief, eligibility is not limited to tech companies or large corporations — small businesses and startups can also qualify.

To qualify, your research activities must:

Aim to create or improve a product, process, formula, or software;

Involve a process of experimentation and technical uncertainty;

Be technological in nature (relying on physical, biological, or computer science principles);

Be conducted within the United States.

Common qualified research expenses include

Wages of employees directly involved in research activities;

Supplies and materials used for experimentation or prototype development;

Contract research expenses paid to third parties.

How to Calculate Your R&D Tax Credit

Now that you understand the basics and know whether your business is eligible, let's explore how to calculate your R&D Tax Credit.

Calculating the R&D Tax Credit can seem complex, but it generally involves identifying your qualified research expenses (QREs) and applying one of two IRS-approved methods: the Regular Credit Calculation or the Alternative Simplified Credit Method.

Here’s a quick comparison:

Method | Overview | Credit Rate | Best For |

Regular Credit Calculation | Based on fixed-base percentage of prior research expenses. | 20% of QREs above the base amount. | Established companies with consistent R&D history. |

Alternative Simplified Credit (ASC) Method | Easier calculation using average of last three years’ QREs. | 14% of QREs exceeding 50% of the average of the previous 3 years. | Startups or businesses without extensive R&D records. |

Steps to Calculate Your R&D Tax Credit:

Identify Qualified Research Expenses (QREs): Include wages, supplies, and contract research costs.

Select a Calculation Method: Choose between the regular or alternative simplified credit method.

Apply the Credit Rate: Multiply eligible expenses by the applicable percentage (20% or 14%).

Example:

Suppose your company has $200,000 in qualified research expenses (QREs).

If you apply a 14% credit rate, your R&D tax credit would be:

$200,000 × 0.14 = $28,000.

Document Everything: Maintain IRS-compliant records to support your calculation.

It’s often best to work with a tax professional to ensure the most accurate computation and maximize your return.

Explore additional insights on Tax Filing Requirements by State to help you prepare supporting documentation.

The Process of Claiming the R&D Tax Credit

Once you’ve determined eligibility and calculated your credit, the next step is to file your claim properly with the IRS.

Step 1: Prepare Documentation

Gather records that clearly demonstrate your R&D activities and associated costs:

Project descriptions, hypotheses, and test results.

Payroll records for employees involved in R&D.

Invoices and receipts for materials and contract research.

Time tracking or engineering logs linking work to specific projects.

Step 2: File Your Claim

To claim the R&D Tax Credit, businesses typically complete IRS Form 6765 and submit it with their annual tax return. Depending on your entity type, you may also need to coordinate with your state’s tax agency, as many states offer parallel R&D incentives.

Callout: Documentation Matters!

Inadequate documentation is one of the most common reasons R&D claims are denied or audited.

Keep detailed, contemporaneous records throughout the year — not just at tax time.

Errors or missing evidence can trigger costly IRS reviews and delay your credit.

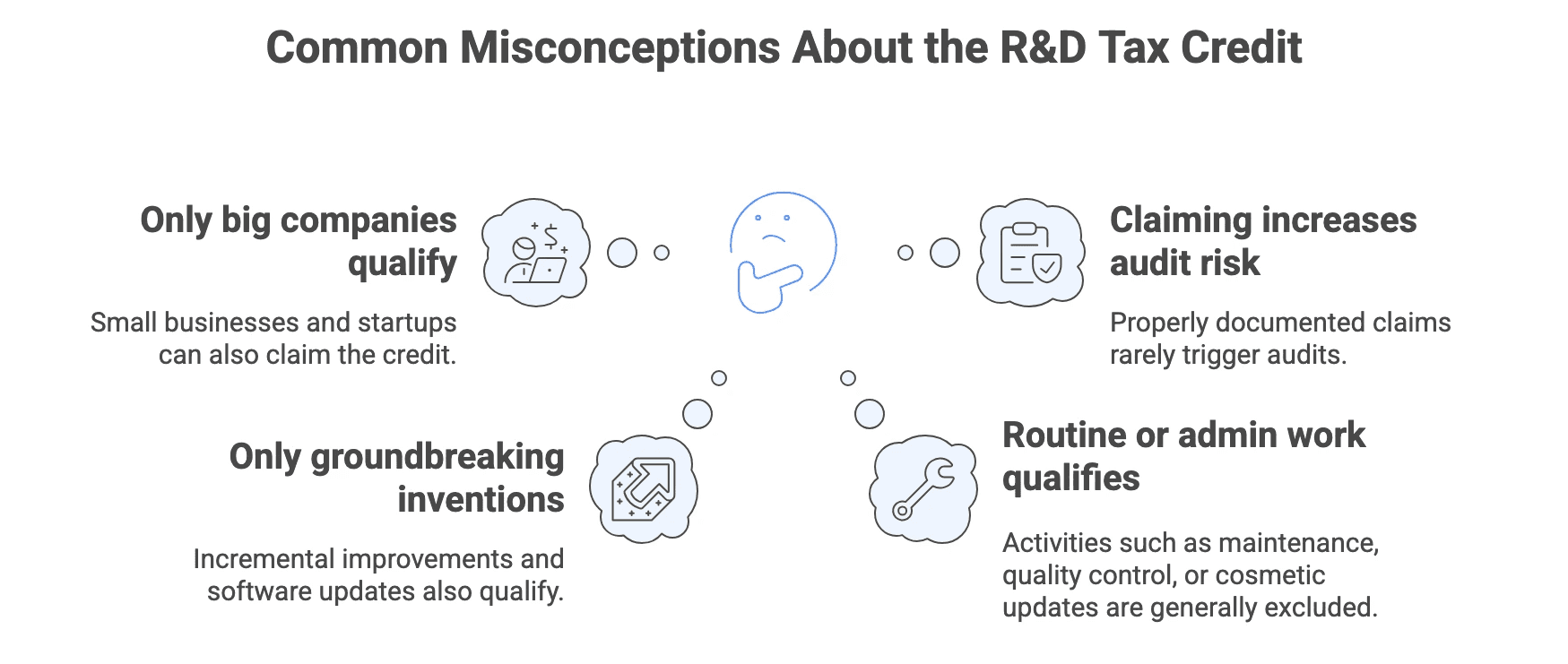

Common R&D Tax Credit Misconceptions

There are several common R&D tax credit misconceptions that prevent companies from taking full advantage of this incentive. Let’s address a few of them:

Myth 1: Only large corporations qualify

Reality: Small businesses and startups can claim the credit, even pre-revenue, if they meet the criteria for eligible activities.

Myth 2: Only groundbreaking inventions count.

Reality: Incremental improvements, software upgrades, and process optimization also qualify — not just revolutionary discoveries.

Myth 3: Administrative or routine tasks qualify.

Reality: Regular maintenance, quality control, and cosmetic design changes are generally excluded.

Myth 4: Claiming the credit increases audit risk.

Reality: While documentation is essential, legitimate claims supported by detailed records rarely trigger audits.

These clarifications help businesses better understand R&D Tax Credit eligibility and confidently file claims that stand up to scrutiny.

Expert Help: How Haven Can Support Your R&D Tax Credit Report

The R&D Tax Credit process requires attention to detail and expert knowledge of IRS criteria. At Haven, our tax professionals specialize in preparing compliant R&D Tax Credit reports — ensuring every qualified research expense is properly documented and maximized.

We can help you:

Assess your R&D Tax Credit eligibility report in detail.

Identify overlooked opportunities within your projects

Prepare IRS-ready documentation to support your claim.

Streamline communication with tax authorities for faster processing.

Partnering with Haven allows your business to focus on innovation while we handle the technical and compliance details of your R&D Tax Credit report.

Frequently Asked Questions (FAQ)

What activities qualify for the R&D tax credit?

Eligible activities involve developing or improving products, processes, or software through experimentation and technical analysis. The key is uncertainty — your project must attempt to resolve a scientific or technological challenge.

Can startups claim R&D tax credit?

Yes. Startups can use the Alternative Simplified Credit Method to claim up to 14% of qualifying expenses, even if they have limited or no tax liability. Some startups can also apply the credit toward payroll taxes.

What documentation is needed to claim the R&D credit?

You’ll need project descriptions, payroll data, material receipts, and time logs that directly connect expenses to qualified research activities. These records help demonstrate compliance with IRS requirements.

Innovation is expensive. The R&D Tax Credit exists to give that money back to founders building something new. The R&D Tax Credit helps startups reinvest in innovation rather than hand that money to the IRS.

In this guide, you’ll learn what the R&D Tax Credit is, who qualifies, how to calculate it, how to claim it properly, and how to avoid common misconceptions that cause companies to miss out on savings.

What Is the R&D Tax Credit?

The R&D Tax Credit is a government incentive designed to stimulate innovation and technological advancement. In the United States, it is administered by the Internal Revenue Service (IRS) and allows eligible businesses to claim a credit for a portion of their qualified research expenses (QREs).

These expenses may include the costs of developing new products, improving manufacturing processes, or experimenting with innovative technologies. The goal is to reduce the financial risk associated with R&D and help companies pursue projects that advance science, technology, and productivity.

Key purposes of the R&D Tax Credit:

Encourage companies to invest in research and innovation;

Stimulate economic growth and high-skilled employment;

Offset some of the costs and uncertainties associated with experimentation.

Eligibility Criteria for the R&D Tax Credit

To claim the R&D Tax Credit, your business must meet certain eligibility requirements defined by the IRS. Contrary to popular belief, eligibility is not limited to tech companies or large corporations — small businesses and startups can also qualify.

To qualify, your research activities must:

Aim to create or improve a product, process, formula, or software;

Involve a process of experimentation and technical uncertainty;

Be technological in nature (relying on physical, biological, or computer science principles);

Be conducted within the United States.

Common qualified research expenses include

Wages of employees directly involved in research activities;

Supplies and materials used for experimentation or prototype development;

Contract research expenses paid to third parties.

How to Calculate Your R&D Tax Credit

Now that you understand the basics and know whether your business is eligible, let's explore how to calculate your R&D Tax Credit.

Calculating the R&D Tax Credit can seem complex, but it generally involves identifying your qualified research expenses (QREs) and applying one of two IRS-approved methods: the Regular Credit Calculation or the Alternative Simplified Credit Method.

Here’s a quick comparison:

Method | Overview | Credit Rate | Best For |

Regular Credit Calculation | Based on fixed-base percentage of prior research expenses. | 20% of QREs above the base amount. | Established companies with consistent R&D history. |

Alternative Simplified Credit (ASC) Method | Easier calculation using average of last three years’ QREs. | 14% of QREs exceeding 50% of the average of the previous 3 years. | Startups or businesses without extensive R&D records. |

Steps to Calculate Your R&D Tax Credit:

Identify Qualified Research Expenses (QREs): Include wages, supplies, and contract research costs.

Select a Calculation Method: Choose between the regular or alternative simplified credit method.

Apply the Credit Rate: Multiply eligible expenses by the applicable percentage (20% or 14%).

Example:

Suppose your company has $200,000 in qualified research expenses (QREs).

If you apply a 14% credit rate, your R&D tax credit would be:

$200,000 × 0.14 = $28,000.

Document Everything: Maintain IRS-compliant records to support your calculation.

It’s often best to work with a tax professional to ensure the most accurate computation and maximize your return.

Explore additional insights on Tax Filing Requirements by State to help you prepare supporting documentation.

The Process of Claiming the R&D Tax Credit

Once you’ve determined eligibility and calculated your credit, the next step is to file your claim properly with the IRS.

Step 1: Prepare Documentation

Gather records that clearly demonstrate your R&D activities and associated costs:

Project descriptions, hypotheses, and test results.

Payroll records for employees involved in R&D.

Invoices and receipts for materials and contract research.

Time tracking or engineering logs linking work to specific projects.

Step 2: File Your Claim

To claim the R&D Tax Credit, businesses typically complete IRS Form 6765 and submit it with their annual tax return. Depending on your entity type, you may also need to coordinate with your state’s tax agency, as many states offer parallel R&D incentives.

Callout: Documentation Matters!

Inadequate documentation is one of the most common reasons R&D claims are denied or audited.

Keep detailed, contemporaneous records throughout the year — not just at tax time.

Errors or missing evidence can trigger costly IRS reviews and delay your credit.

Common R&D Tax Credit Misconceptions

There are several common R&D tax credit misconceptions that prevent companies from taking full advantage of this incentive. Let’s address a few of them:

Myth 1: Only large corporations qualify

Reality: Small businesses and startups can claim the credit, even pre-revenue, if they meet the criteria for eligible activities.

Myth 2: Only groundbreaking inventions count.

Reality: Incremental improvements, software upgrades, and process optimization also qualify — not just revolutionary discoveries.

Myth 3: Administrative or routine tasks qualify.

Reality: Regular maintenance, quality control, and cosmetic design changes are generally excluded.

Myth 4: Claiming the credit increases audit risk.

Reality: While documentation is essential, legitimate claims supported by detailed records rarely trigger audits.

These clarifications help businesses better understand R&D Tax Credit eligibility and confidently file claims that stand up to scrutiny.

Expert Help: How Haven Can Support Your R&D Tax Credit Report

The R&D Tax Credit process requires attention to detail and expert knowledge of IRS criteria. At Haven, our tax professionals specialize in preparing compliant R&D Tax Credit reports — ensuring every qualified research expense is properly documented and maximized.

We can help you:

Assess your R&D Tax Credit eligibility report in detail.

Identify overlooked opportunities within your projects

Prepare IRS-ready documentation to support your claim.

Streamline communication with tax authorities for faster processing.

Partnering with Haven allows your business to focus on innovation while we handle the technical and compliance details of your R&D Tax Credit report.

Frequently Asked Questions (FAQ)

What activities qualify for the R&D tax credit?

Eligible activities involve developing or improving products, processes, or software through experimentation and technical analysis. The key is uncertainty — your project must attempt to resolve a scientific or technological challenge.

Can startups claim R&D tax credit?

Yes. Startups can use the Alternative Simplified Credit Method to claim up to 14% of qualifying expenses, even if they have limited or no tax liability. Some startups can also apply the credit toward payroll taxes.

What documentation is needed to claim the R&D credit?

You’ll need project descriptions, payroll data, material receipts, and time logs that directly connect expenses to qualified research activities. These records help demonstrate compliance with IRS requirements.

This article was co-written by:

Content

This article was co-written by:

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.