Go Back

Last Updated :

Last Updated :

Nov 7, 2025

Nov 7, 2025

R&D Tax Credits for Manufacturing: Maximize Benefits & Stay Compliant

The R&D Tax Credit for manufacturing helps companies offset the high cost of innovation. This federal incentive rewards businesses that invest in research and development activities to improve their processes or products.

While many assume the credit only applies to tech companies, manufacturers are actually among its biggest beneficiaries — often without realizing it. From prototyping to process optimization, many day-to-day improvements already qualify for this powerful incentive under IRS Section 41 (R&D Tax Credit) and Section 174 (capitalization rules for R&D expenses).

Why the R&D Tax Credit Matters for Manufacturers

Innovation is expensive; the R&D Tax Credit helps offset those costs, freeing up capital to reinvest in growth, new technology, or workforce development.

Manufacturers can apply the credit against both federal and state tax liabilities, and in some cases (for qualified small businesses or startups), even use it to offset payroll taxes — a major advantage for companies still scaling or reinvesting aggressively.

Don’t Leave Money on the Table

Many manufacturing businesses miss out on R&D credits simply because they assume they don’t qualify. However, if your company is solving technical challenges, improving production processes, or enhancing product quality, you likely already meet the criteria.

By working with professionals who understand the nuances of Section 41 (qualified research) and Section 174 (amortization rules), you can:

Identify qualifying R&D activities

Properly document your efforts

Claim the maximum benefit available

How to Qualify for the R&D Tax Credit for Manufacturing

If your manufacturing business invests in developing new products, improving processes, or building prototypes, you may already qualify for the R&D Tax Credit — even if you haven’t claimed it before.

To be eligible, your activities must meet the IRS’s four-part test, along with some manufacturing-specific requirements.

The Four-Part Test for R&D Credit Eligibility

The IRS requires that qualifying research activities meet all four criteria below:

1. Product or Process Improvement

Your work must aim to improve the function, performance, reliability, or quality of a product or production process. This could include:

New product development

Process optimization

Prototyping and iterative testing

Efforts involving reverse engineering, simple customization, or modifications at a customer’s request generally do not qualify.

2. Technological in Nature

Research must rely on principles of the hard sciences, such as:

Engineering

Physics

Chemistry

Computer science

Activities based on social sciences or business processes (e.g., marketing, finance, or management) are excluded.

3. Technical Uncertainty

You must have faced uncertainty during the project — not knowing if or how a product or process could be developed or improved. This can include uncertainty in:

Capability

Method

Design

4. Process of Experimentation

You must show evidence of systematic experimentation or a trial-and-error process to resolve the uncertainty. Examples include:

Prototyping

Modeling

Testing

Iterative development cycles

For manufacturers, having a formal product development lifecycle or quality assurance workflow often supports this requirement.

Key Considerations for Manufacturers

Time and Activity Tracking

Accurate tracking is critical. Engineers often log hours by project, but teams like tooling, QA, or prototyping may not. Make sure every employee involved in qualifying activities understands what counts — and document their contributions accordingly.

IRC Section 174 & Pilot Models

Under Section 174, supply costs associated with pilot models used for evaluation or testing can qualify. Maintaining detailed documentation on pilot model designs and testing phases can unlock substantial supply cost credits.

ASC 730 Safe Harbor (For Large Manufacturers)

If your business uses U.S. GAAP and prepares financial statements, the ASC 730 Safe Harbor method may simplify your claim. It allows the use of financial reporting R&D expenses as a basis for the credit, reducing the administrative burden of project-level tracking.

Qualified Startup Payroll Offset

If your company is a qualified small business (under $5 million in gross receipts and within its first five years of revenue), you can apply up to $500,000 in R&D Tax Credits against payroll taxes — even if you’re not yet profitable.

Be sure to check “controlled group” status to confirm total receipts remain under the $5 million threshold.

AMT Offset

For tax years beginning after December 31, 2015, small businesses with $50 million or less in gross receipts can use the R&D Tax Credit to offset Alternative Minimum Tax (AMT) liability.

State-Level R&D Credits

Many states offer R&D tax incentives, with some allowing refunds or transfers even if you owe no income tax. Rules vary by state, but programs in New Jersey, Massachusetts, and others have simplified their credit calculations — making access easier.

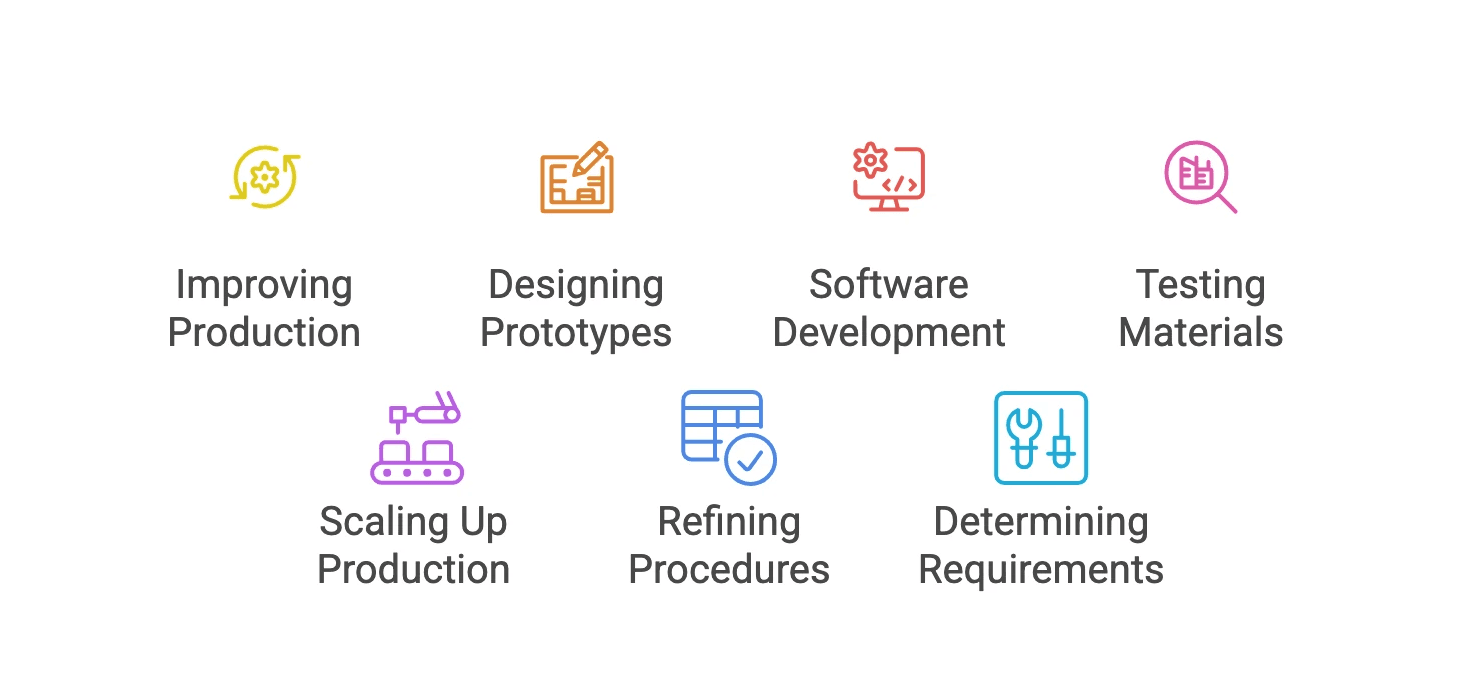

Examples of Qualifying R&D Activities

The scope of qualifying R&D is broader than most manufacturers expect. Activities that improve a product or process — while involving technical uncertainty and experimentation — may qualify.

Examples include:

Improving production efficiency through automation or lean processes

Designing and prototyping new products or tools

Developing or customizing internal software (e.g., manufacturing execution systems)

Testing new materials to reduce costs or improve durability

Scaling up from prototype to full production

Refining QA or inspection procedures

Determining tooling and equipment requirements

Meeting new regulatory or compliance standards

Developing robotics or advanced automation systems

Experimenting with new filling or packaging techniques

Even failed projects can qualify — what matters is that you attempted to solve a technical challenge using a structured, science-based approach.

Recent Changes Regarding Section 174 and How They Affect Manufacturers

The Game-Changer: R&D Capitalization

The Tax Cuts and Jobs Act (TCJA), passed in 2017, changed how manufacturers handle R&D expenses under Section 174. Starting with tax years after December 31, 2021, businesses can no longer fully deduct qualifying R&D expenses in the year incurred.

The Key Change: No More Immediate Deduction

Previously, R&D costs could be deducted in full during the year they occurred. Now, they must be capitalized and amortized over time:

5 years for U.S.-based R&D

15 years for foreign R&D

This shift means only about 10% of domestic R&D costs can be deducted in the first year, delaying the tax benefit and potentially tightening cash flow.

Aspect | Pre-2022 Section 174 (Before TCJA) | Post-2022 Section 174 (Effective 2022) |

Treatment of R&D Expenses | Immediate full deduction | Mandatory capitalization & amortization |

Amortization Period | Not applicable | 5 years (domestic), 15 years (foreign) |

Impact on Cash Flow | Immediate tax benefit | Delayed benefit; reduced short-term cash flow |

Planning Implications | Simple | Requires strategic tracking and compliance |

Why This Matters for Manufacturers?

Manufacturers often perform R&D as part of product design, process improvement, or materials testing — all of which fall under Section 174.

Under the new rules, these expenses increase taxable income in the short term, leading to higher tax bills even without operational changes. This shift affects cash flow, forecasting, and capital planning, especially for equipment-heavy operations.

How R&D Tax Credits Help Offset the Impact

While the new Section 174 rules create short-term tax pressure, manufacturers can still leverage Section 41 R&D Tax Credits to offset the impact.

These credits provide a dollar-for-dollar reduction in tax liability, mitigating the effects of capitalization.

In short:

If you’re now required to amortize R&D costs, you should also be optimizing your R&D tax credit strategy.

Although credits can’t eliminate capitalization rules, they can significantly reduce your total tax burden and improve long-term ROI.

What’s Next?

Ongoing legislative efforts — including the American Innovation and R&D Competitiveness Act of 2025 — aim to restore immediate expensing for R&D costs. If enacted, this could reverse the Section 174 amortization requirement, reinstating full deductions.

Until then, manufacturers should:

Accurately identify and classify Specified Research or Experimental (SRE) expenses

Ensure Section 174 compliance in filings

Maximize Section 41 R&D Credits to reduce liability

Monitor legislative updates impacting future filings

Proactive planning can minimize the downside while positioning your business to benefit when regulations shift.

Maximizing Your R&D Tax Credits

Treating the R&D credit as a year-round strategy — not just a tax-season task — helps unlock its full potential.

Commonly Overlooked Activities

R&D isn’t limited to lab work. Many manufacturing and engineering improvements qualify, including:

Software development for production control

Process optimization or automation

Product testing and iteration

Prototyping and tooling design

Documentation is Everything

Good documentation supports your credit and protects you in the event of an audit. Track:

R&D objectives and outcomes

Technical challenges

Experimentation steps

Related costs (materials, wages, contractors)

Partner with R&D Tax Credit Experts

Tax law is complex. Partnering with specialists helps ensure compliance and maximizes your claim. Experts can structure your documentation, identify overlooked activities, and help you claim credits across multiple tax years or states.

Make R&D Tax Credits Part of Your Annual Strategy

Integrate R&D tax credit management into your annual financial and operational planning. Stay proactive by:

Reviewing and updating qualifying activities yearly

Tracking tax law changes under Sections 41 and 174

Maintaining organized documentation and project logs

Consulting professionals for compliance and strategic planning

Factoring R&D credits into budgets and cash flow forecasts

Building this into your yearly routine ensures your innovation translates into measurable financial benefit.

Learn More About Our Accounting Services

At Haven, we help startups and growing businesses navigate complex R&D regulations — from capitalization under Section 174 to payroll offsets and compliance strategies.

Our team can help you manage your accounting confidently while maximizing every available credit.

The R&D Tax Credit for manufacturing helps companies offset the high cost of innovation. This federal incentive rewards businesses that invest in research and development activities to improve their processes or products.

While many assume the credit only applies to tech companies, manufacturers are actually among its biggest beneficiaries — often without realizing it. From prototyping to process optimization, many day-to-day improvements already qualify for this powerful incentive under IRS Section 41 (R&D Tax Credit) and Section 174 (capitalization rules for R&D expenses).

Why the R&D Tax Credit Matters for Manufacturers

Innovation is expensive; the R&D Tax Credit helps offset those costs, freeing up capital to reinvest in growth, new technology, or workforce development.

Manufacturers can apply the credit against both federal and state tax liabilities, and in some cases (for qualified small businesses or startups), even use it to offset payroll taxes — a major advantage for companies still scaling or reinvesting aggressively.

Don’t Leave Money on the Table

Many manufacturing businesses miss out on R&D credits simply because they assume they don’t qualify. However, if your company is solving technical challenges, improving production processes, or enhancing product quality, you likely already meet the criteria.

By working with professionals who understand the nuances of Section 41 (qualified research) and Section 174 (amortization rules), you can:

Identify qualifying R&D activities

Properly document your efforts

Claim the maximum benefit available

How to Qualify for the R&D Tax Credit for Manufacturing

If your manufacturing business invests in developing new products, improving processes, or building prototypes, you may already qualify for the R&D Tax Credit — even if you haven’t claimed it before.

To be eligible, your activities must meet the IRS’s four-part test, along with some manufacturing-specific requirements.

The Four-Part Test for R&D Credit Eligibility

The IRS requires that qualifying research activities meet all four criteria below:

1. Product or Process Improvement

Your work must aim to improve the function, performance, reliability, or quality of a product or production process. This could include:

New product development

Process optimization

Prototyping and iterative testing

Efforts involving reverse engineering, simple customization, or modifications at a customer’s request generally do not qualify.

2. Technological in Nature

Research must rely on principles of the hard sciences, such as:

Engineering

Physics

Chemistry

Computer science

Activities based on social sciences or business processes (e.g., marketing, finance, or management) are excluded.

3. Technical Uncertainty

You must have faced uncertainty during the project — not knowing if or how a product or process could be developed or improved. This can include uncertainty in:

Capability

Method

Design

4. Process of Experimentation

You must show evidence of systematic experimentation or a trial-and-error process to resolve the uncertainty. Examples include:

Prototyping

Modeling

Testing

Iterative development cycles

For manufacturers, having a formal product development lifecycle or quality assurance workflow often supports this requirement.

Key Considerations for Manufacturers

Time and Activity Tracking

Accurate tracking is critical. Engineers often log hours by project, but teams like tooling, QA, or prototyping may not. Make sure every employee involved in qualifying activities understands what counts — and document their contributions accordingly.

IRC Section 174 & Pilot Models

Under Section 174, supply costs associated with pilot models used for evaluation or testing can qualify. Maintaining detailed documentation on pilot model designs and testing phases can unlock substantial supply cost credits.

ASC 730 Safe Harbor (For Large Manufacturers)

If your business uses U.S. GAAP and prepares financial statements, the ASC 730 Safe Harbor method may simplify your claim. It allows the use of financial reporting R&D expenses as a basis for the credit, reducing the administrative burden of project-level tracking.

Qualified Startup Payroll Offset

If your company is a qualified small business (under $5 million in gross receipts and within its first five years of revenue), you can apply up to $500,000 in R&D Tax Credits against payroll taxes — even if you’re not yet profitable.

Be sure to check “controlled group” status to confirm total receipts remain under the $5 million threshold.

AMT Offset

For tax years beginning after December 31, 2015, small businesses with $50 million or less in gross receipts can use the R&D Tax Credit to offset Alternative Minimum Tax (AMT) liability.

State-Level R&D Credits

Many states offer R&D tax incentives, with some allowing refunds or transfers even if you owe no income tax. Rules vary by state, but programs in New Jersey, Massachusetts, and others have simplified their credit calculations — making access easier.

Examples of Qualifying R&D Activities

The scope of qualifying R&D is broader than most manufacturers expect. Activities that improve a product or process — while involving technical uncertainty and experimentation — may qualify.

Examples include:

Improving production efficiency through automation or lean processes

Designing and prototyping new products or tools

Developing or customizing internal software (e.g., manufacturing execution systems)

Testing new materials to reduce costs or improve durability

Scaling up from prototype to full production

Refining QA or inspection procedures

Determining tooling and equipment requirements

Meeting new regulatory or compliance standards

Developing robotics or advanced automation systems

Experimenting with new filling or packaging techniques

Even failed projects can qualify — what matters is that you attempted to solve a technical challenge using a structured, science-based approach.

Recent Changes Regarding Section 174 and How They Affect Manufacturers

The Game-Changer: R&D Capitalization

The Tax Cuts and Jobs Act (TCJA), passed in 2017, changed how manufacturers handle R&D expenses under Section 174. Starting with tax years after December 31, 2021, businesses can no longer fully deduct qualifying R&D expenses in the year incurred.

The Key Change: No More Immediate Deduction

Previously, R&D costs could be deducted in full during the year they occurred. Now, they must be capitalized and amortized over time:

5 years for U.S.-based R&D

15 years for foreign R&D

This shift means only about 10% of domestic R&D costs can be deducted in the first year, delaying the tax benefit and potentially tightening cash flow.

Aspect | Pre-2022 Section 174 (Before TCJA) | Post-2022 Section 174 (Effective 2022) |

Treatment of R&D Expenses | Immediate full deduction | Mandatory capitalization & amortization |

Amortization Period | Not applicable | 5 years (domestic), 15 years (foreign) |

Impact on Cash Flow | Immediate tax benefit | Delayed benefit; reduced short-term cash flow |

Planning Implications | Simple | Requires strategic tracking and compliance |

Why This Matters for Manufacturers?

Manufacturers often perform R&D as part of product design, process improvement, or materials testing — all of which fall under Section 174.

Under the new rules, these expenses increase taxable income in the short term, leading to higher tax bills even without operational changes. This shift affects cash flow, forecasting, and capital planning, especially for equipment-heavy operations.

How R&D Tax Credits Help Offset the Impact

While the new Section 174 rules create short-term tax pressure, manufacturers can still leverage Section 41 R&D Tax Credits to offset the impact.

These credits provide a dollar-for-dollar reduction in tax liability, mitigating the effects of capitalization.

In short:

If you’re now required to amortize R&D costs, you should also be optimizing your R&D tax credit strategy.

Although credits can’t eliminate capitalization rules, they can significantly reduce your total tax burden and improve long-term ROI.

What’s Next?

Ongoing legislative efforts — including the American Innovation and R&D Competitiveness Act of 2025 — aim to restore immediate expensing for R&D costs. If enacted, this could reverse the Section 174 amortization requirement, reinstating full deductions.

Until then, manufacturers should:

Accurately identify and classify Specified Research or Experimental (SRE) expenses

Ensure Section 174 compliance in filings

Maximize Section 41 R&D Credits to reduce liability

Monitor legislative updates impacting future filings

Proactive planning can minimize the downside while positioning your business to benefit when regulations shift.

Maximizing Your R&D Tax Credits

Treating the R&D credit as a year-round strategy — not just a tax-season task — helps unlock its full potential.

Commonly Overlooked Activities

R&D isn’t limited to lab work. Many manufacturing and engineering improvements qualify, including:

Software development for production control

Process optimization or automation

Product testing and iteration

Prototyping and tooling design

Documentation is Everything

Good documentation supports your credit and protects you in the event of an audit. Track:

R&D objectives and outcomes

Technical challenges

Experimentation steps

Related costs (materials, wages, contractors)

Partner with R&D Tax Credit Experts

Tax law is complex. Partnering with specialists helps ensure compliance and maximizes your claim. Experts can structure your documentation, identify overlooked activities, and help you claim credits across multiple tax years or states.

Make R&D Tax Credits Part of Your Annual Strategy

Integrate R&D tax credit management into your annual financial and operational planning. Stay proactive by:

Reviewing and updating qualifying activities yearly

Tracking tax law changes under Sections 41 and 174

Maintaining organized documentation and project logs

Consulting professionals for compliance and strategic planning

Factoring R&D credits into budgets and cash flow forecasts

Building this into your yearly routine ensures your innovation translates into measurable financial benefit.

Learn More About Our Accounting Services

At Haven, we help startups and growing businesses navigate complex R&D regulations — from capitalization under Section 174 to payroll offsets and compliance strategies.

Our team can help you manage your accounting confidently while maximizing every available credit.

This article was co-written by:

Content

This article was co-written by:

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.

2026

© Haven All Rights Reserved

Haven is a financial technology company, not an FDIC-insured bank. Banking services are provided by OMB Bank, Member FDIC. Deposits in checking and savings accounts are held at OMB Bank and are insured by the FDIC up to the applicable limits. FDIC insurance covers the failure of an insured bank. Certain conditions must be met for pass-through insurance coverage to apply. Fees, terms, and conditions apply to depositing and using your account.